What Is Employer Coverage Enough? 7 Real Case Examples Exposing Critical Gaps in 2026. Is organization fitness insurance sufficient in 2026? Discover 7 actual case examples revealing risky gaps in organization coverage, out-of-pocket charges & scientific debt.

7 Real Case Examples Exposing Critical Gaps in 2026: Is Employer Coverage Enough?

Introduction

Employment-primarily based totally medical insurance is the maximum not unusual place shape of fitness insurance with inside the United States, shielding 53.8% of the populace for a few or all of 2024, consistent with the U.S. Census Bureau`s Current Population Survey (2025). Yet sporting an organization-subsidized coverage card does now no longer assure well enough economic safety.

The Commonwealth Fund’s 2024 Biennial Health Insurance Survey determined that a couple of in 5 working-age adults are underinsured — which means their insurance, despite its existence, leaves them uncovered to deductibles and out-of-pocket charges they cannot realistically afford. The query is now no longer genuinely whether or not Americans have coverage. The pressing query is: does that coverage certainly, paintings while its topics maximum?

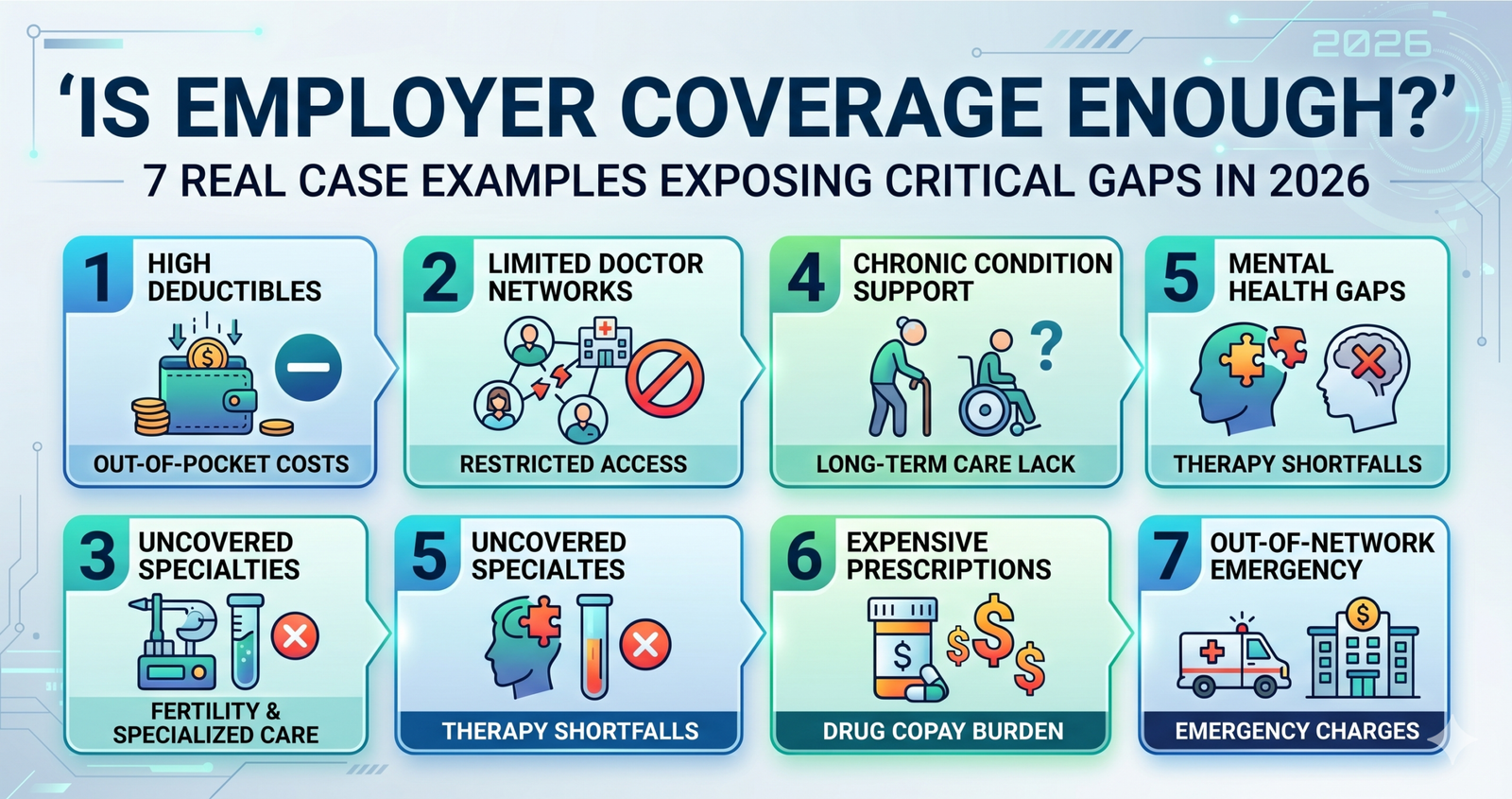

Real Case Examples and the Gaps Employer Coverage Leaves Behind

Case 1: The Worker with Insurance Who Still Faced $20,000 in Medical Debt

George, a complete-time warehouse employee close to Dallas, Texas, suffered a business coincidence at the job. Despite his organization being legally accountable for the damage and George sporting organization-subsidized medical insurance, he nevertheless accrued greater than $20,000 in scientific debt following surgical treatment and the amputation of one in all his toes.

His story, documented via way of means of the Cornell ILR School, illustrates a difficult reality: even if coverage and workers’ repayment intersect, surprising out-of-pocket charges, gaps in insurance, and time far from paintings can integrate to create a economic catastrophe. His scientific debt dropped his credit score rating via way of means of 60 points, avoided him from renting his personal home, and derailed his profession plans — all even as he remained hired and insured.

This case is not exceptional. According to the Cornell ILR School’s healthcare analysis, 80% of Americans who bring scientific debt are insured, and maximum are hired. Coverage gaps along with out-of-community charges, exposed procedures, and ambulance transport — that is not often protected in complete via way of means of organization plans — are a few of the maximum not unusual place triggers for insured scientific debt. The gadget designed to guard human beings like George regularly fails them at exactly the instant they want safety maximum.

Case 2: The Breast Cancer Survivor Left without Care by Coverage Transitions

Penelope Wingard, a 58-year-antique woman from Charlotte, North Carolina, illustrates what takes place while enterprise and public insurance collide unpredictably. After present process breast most cancers remedy even as blanketed via way of means of Medicaid, she eventually misplaced that insurance and determined herself dealing with the overall monetary weight of ongoing oncology comply with-up care without good enough coverage. As documented in reporting at the U.S. scientific debt crisis, she defined being not able to peer her oncologist earlier than her hair had even grown again from chemotherapy — a stark human result of insurance gaps that enterprise-primarily based totally plans and transitional coverage applications mechanically fail to close.

Her case exposes a structural flaw: Americans whose insurance modifications because of employment transitions, earnings fluctuations, or lifestyles occasions regularly fall via the areas among coverage types. Employer insurance does now no longer comply with people after they lose their jobs, lessen their hours, or pass among employers — and the value of endured insurance via COBRA is frequently prohibitive. According to KFF`s 2025 Employer Health Benefits Survey, common annual charges for enterprise-backed own circle of relatives fitness insurance reached $26,993 in 2025, a 6% growth from 2024. Workers who abruptly endure that complete value for the duration of an activity transition usually cannot maintain it.

Case 3: The Low-Income Family Paying Nearly 10% of Income Just for Health Costs

Among the maximum invisible types of coverage inadequacy is the load carried via way of means of lower-earnings households with enterprise insurance. The Peterson-KFF Health System Tracker (2025) determined that for households with earning at or beneath 199% of the federal poverty stage who have enterprise-primarily based very insurance, the common own circle of relatives bills for medical insurance charges and out-of-pocket scientific costs eat 9.6% of own circle of relatives earnings. That discerns rises sharply while any member of the family is in honest or terrible fitness, attaining fees that no affordable family price range can take in sustainably.

The Affordable Care Act calls for employers with extra than 50 personnel to provide insurance that is “affordable,” described as requiring worker contributions of much less than 9.5% of family earnings for self-handiest insurance in 2025. However, the ACA’s affordability trendy applies handiest to the worker’s personal insurance — now no longer to base insurance. An own circle of relatives with youngsters enrolled in enterprise-backed insurance might also additionally face contributions deemed unaffordable via way of means of any realistic trendy even as being technically ineligible for market subsidies. This hole traps hundreds of thousands of low-earnings households in coverage plans that value them proportionally a long way extra than they values better earners, even as imparting them no prison recourse.

Case 4: The High-Deductible Plan That Was No Plan at All in an Emergency

High-deductible fitness plans (HDHPs) have emerge as the dominant shape of company-subsidized insurance, pushed via way of means of company cost-moving strategies. The American Hospital Association notes that the common widespread annual deductible for unmarried, company-subsidized insurance exceeds $1, four hundred — and a Federal Reserve file discovered that 37% of adults could not have the funds for a $four hundred emergency expense, and quantity a ways much less than maximum HDHP deductibles. The common sense is simple and devastating: tens of thousands and thousands of Americans convey coverage so one can now no longer cowl a unmarried greenback of care till they’ve in my opinion spent extra money than they’ve.

In realistic terms, which means an employee with an HDHP who develops appendicitis, breaks a bone, or stories a cardiac occasion faces a desire among in search of important care and assuming heaps of bucks in out-of-pocket prices, or delaying care and risking their fitness. According to Johns Hopkins Bloomberg School of Public Health (2026), in any given 12 months approximately 20% of Americans will revel in a prime scientific expenditure — usually greater than $5,000, growing to $20,000 or greater for a hospitalization. For the tens of thousands and thousands enrolled in excessive-deductible company plans without ok savings, the economic safety their insurance theoretically gives stays efficaciously unreachable.

Case 5: The Employee Blindsided via way of means of Out-of-Network Billing

Even employees with complete company insurance often face wonder payments while the care they acquire is introduced via way of means of vendors outdoor their plan`s community. The Cornell ILR School’s evaluation files how, at some stage in catastrophic events, sufferers are regularly transported to centers or handled via way of means of vendors outdoor their community — now no longer via way of means of desire, however via way of means of circumstance. Emergency transport, expert specialists with inside the running room, anesthesiologists, and radiologists may also all be out-of-community even if a health facility itself is in-community, producing payments, the affected person had no manner to count on or prevent.

The Roosevelt Institute’s 2025 evaluation of U.S. scientific debt confirms that coverage plans might not cowl care obtained at out-of-community centers, may also require big co-can pay for health facility stays, and convey excessive deductibles that should be met earlier than insurance activates — all of which flip what have to be an economic backstop right into a partial and unpredictable safety. Most fitness plans cowl simplest 80% of prices even for blanketed services, leaving a 20% affected person duty that could translate to tens of heaps of bucks in a critical scientific occasion.

Case 6: The Part-Time Worker with No Access to Employer Benefits

Not all people get hold of it gets right of entry to enterprise-backed insurance. The U.S. Census Bureau`s 2024 fitness insurance information display that part-time people have an uninsured charge of 13.4%, as compared to 8.8% amongst full-time people. In occupations, which include farming, fishing, and forestry, the uninsured charge amongst people reaches 29.4% — almost one in three — notwithstanding the ones people being actively employed? Even in healthcare aid roles, 10.5% of people continue to be uninsured, greater than two times the charge in their scientific opposite numbers with inside the equal facilities.

The enterprise provide charge in 2024 stood at 65% amongst companies with 10 or greater employees, that means greater than a 3rd of smaller employers provide no insurance at all, in step with KFF’s 2025 Employer Health Benefits Survey. Workers in those environments — regularly in low-wage, bodily demanding, or seasonal roles — are left to navigate highly priced person marketplace alternatives or continue to be uninsured. For those people, the idea that employment ensures fitness protection does now no longer replicate the shape of the American exertions marketplace because it really functions.

Case 7: The Underinsured Employee Who Delayed Care Until It Was Too Late

Perhaps the maximum insidious result of insufficient enterprise insurance is the behavioral sample it creates: the selection to put off or forgo essential care due to expected cost. The Roosevelt Institute’s 2025 scientific debt evaluation files that the Commonwealth Fund located 23% of working-age adults with regular coverage insurance have been underinsured in 2024, and that underinsurance discourages preventive care — accelerating the very fitness crises that generate catastrophic expenses later. Johns’ Hopkins public fitness researchers referred to in January 2026 that human beings with scientific debt are 5 instances much more likely to forgo intellectual fitness care than the ones without debt.

An expected 60–65% of private bankruptcies with inside the United States are tied to unpaid scientific bills, in step with Johns Hopkins Bloomberg School of Public Health (2026). Medical debt isn’t always a trouble of the uninsured — it’s miles a trouble of the inadequately insured, and enterprise insurance, notwithstanding its large attain and structural advantages, regularly qualifies as insufficient with the aid of using the instant an employee faces a proper fitness crisis.

Conclusion

Employer medical health insurance stays the spine of American fitness insurance, however the proof of 2024 and 2025 makes unmistakably clean that having insurance and being blanketed are not the equal thing. From the warehouse employee who owed $20,000 after a job-associated damage to the most cancers survivor who couldn`t have the funds for follow-up oncology care, actual instances illustrate what records confirm: excessive deductibles, out-of-community billing, affordability gaps for lower-earnings families, and part-time employment exclusions together undermine the safety that corporation insurance is thought to offer.

For employees, this indicates corporation insurance must be evaluated critically — now no longer widely widespread passively. Understanding your deductible, most out-of-pocket prices, community breadth, and the price of based insurance earlier than a fitness disaster move isn’t always elective monetary literacy — it’s far crucial self-safety. For researchers, educators, and coverage advocates, those instances underscore that insurance reform must deal with now no longer best who has coverage however what that coverage certainly covers, and whether its prices are proportionate to what employees can realistically bear.

FAQs

What percent of Americans with corporation insurance are taken into consideration underinsured?

According to the Commonwealth Fund’s 2024 Biennial Health Insurance Survey, 23% of working-age adults with constant medical health insurance had been underinsured — that means their deductibles or out-of-pocket prices had been excessive sufficient relative to their earnings to depart them without significant monetary safety.

How a great deal did corporation-backed own circle of relative’s fitness insurance price on common in 2025?

According to KFF’s 2025 Employer Health Benefits Survey, common annual charges for corporation-backed own circle of relative’s fitness insurance reached $26,993 in 2025, a 6% growth over 2024. Workers contributed a mean of $6,850 towards that own circle of relative’s top rate price.

Can I even have corporation medical health insurance and nonetheless face scientific bankruptcy?

Yes. Johns Hopkins Bloomberg School of Public Health researchers estimate that 60–65% of private bankruptcies with inside the United States are tied to scientific bills, and the bulk of these people had been insured. High deductibles, out-of-community charges, and exposed offerings are the maximum not unusual place drivers of insured scientific debt and monetary disaster.

What need to employees do if they assume their corporation insurance is insufficient?

Workers need to assessment their plan’s annual deductible, out-of-pocket most, community directory, and based insurance prices throughout open enrollment. Supplemental coverage, Health Savings Accounts (HSAs), or market plan comparisons may also offer extra safety. Consulting with a certified coverage-marketing consultant is a sensible subsequent step for people with continual situations or dependents with ongoing healthcare needs.

Read More:

https://nurseseducator.com/didactic-and-dialectic-teaching-rationale-for-team-based-learning/

https://nurseseducator.com/high-fidelity-simulation-use-in-nursing-education/

First NCLEX Exam Center In Pakistan From Lahore (Mall of Lahore) to the Global Nursing

Categories of Journals: W, X, Y and Z Category Journal In Nursing Education

AI in Healthcare Content Creation: A Double-Edged Sword and Scary

Social Links:

https://www.facebook.com/nurseseducator/

https://www.instagram.com/nurseseducator/

https://www.pinterest.com/NursesEducator/

https://www.linkedin.com/company/nurseseducator/

https://www.linkedin.com/in/afzalaldin/

https://www.researchgate.net/profile/Afza-Lal-Din

https://scholar.google.com/citations?hl=en&user=F0XY9vQAAAAJ