Learning How to Choose the Best Malpractice Insurance Plan for Nurses in 2026: 9 Critical Factors. A way to select the quality malpractice coverage plan for nurses in 2025. Compare prevalence vs. claims-made policies, insurance limits, costs, and pinnacle providers.

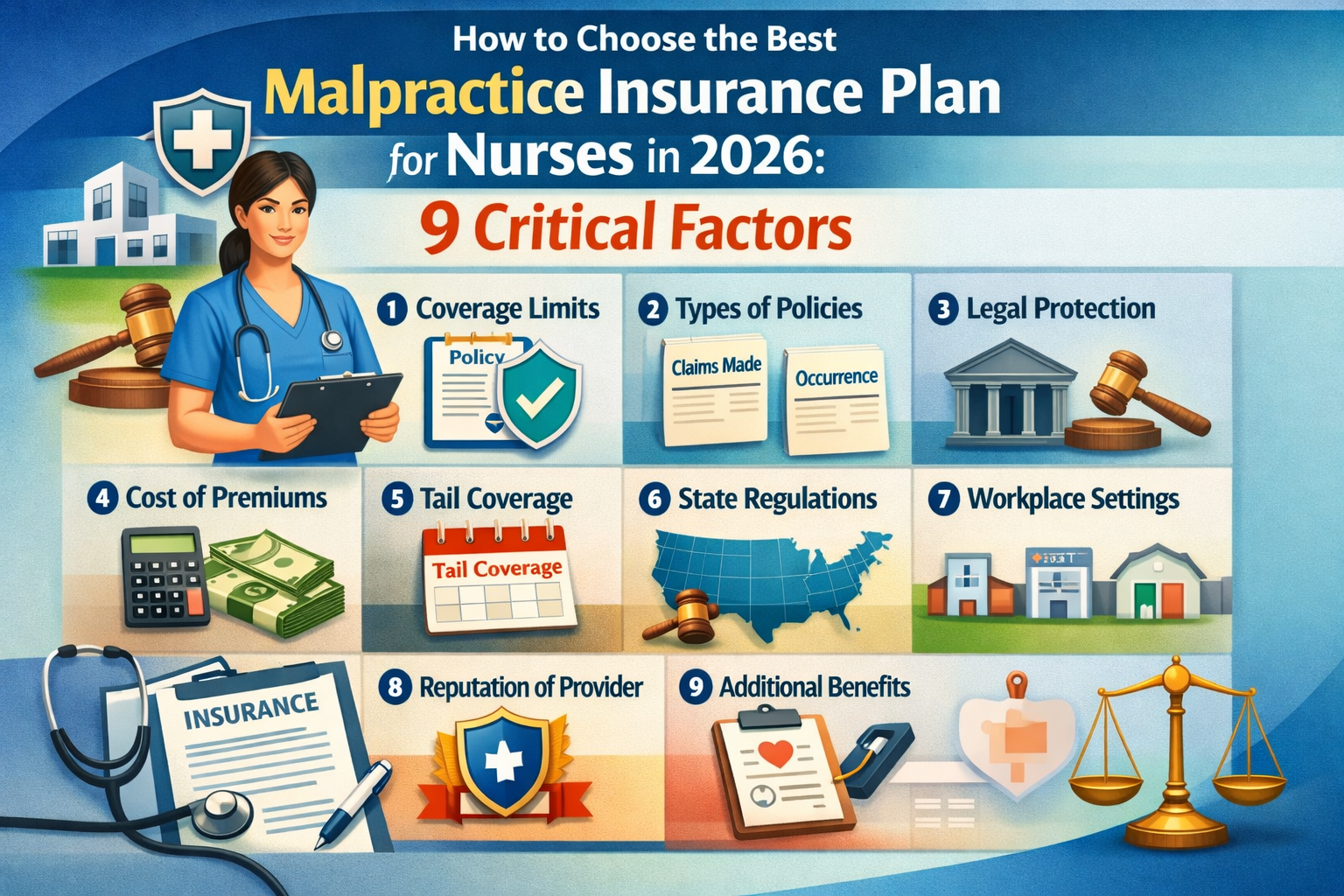

9 Critical Factors: How to Choose the Best Malpractice Insurance Plan for Nurses in 2026

Introduction

Nursing malpractice coverage is not always a luxury — it is far an expert lifeline. The common scientific malpractice payout with inside the United States has reached $329,565, with massive verdicts exceeding $five million turning into more and more common (thecredentialing.com, 2025). Yet a placing wide variety of nurses depend totally on their company`s coverage, unaware that institutional insurance is designed to shield the agency first — now no longer the man or woman nurse.

Whether you’re a new graduate RN, a pro nurse practitioner, or a complicated exercise clinician transitioning to impartial exercise, choosing the proper malpractice coverage plan calls for know-how coverage structures, insurance limits, specialty-precise risks, and the important differences that decide whether or not you’re clearly included or dangerously uncovered whilst a declare arises.

Why Every Nurse Needs Individual Malpractice Insurance

One of the maximum persistent — and costly — misconceptions in nursing is that company-supplied malpractice insurance is sufficient. It is not always. Nurse legal professional Nancy J. Brent, MS, JD, RN, writer of Nurses and the Law, states clearly: “I actually have represented NPs who did now no longer have sufficient coverage, or who have been handiest protected via way of means of their company, and who were given in problem with the board of nursing, and observed themselves in a huge heap of a mess. If they’d their personal malpractice coverage, they would not be in a heap of a mess.”

The essential hassle with company-supplied insurance is structural: it has far written to shield the institution, now no longer the man or woman clinician. If a company believes a nurse can also additionally endure private legal responsibility for a declaration, the identical institutional coverage will be used towards that nurse in a counterclaim.

Moreover, company-supplied plans nearly universally exclude Board of Nursing lawsuits and disciplinary proceedings — regularly the maximum instantaneously and career-threatening criminal threat a nurse without a doubt faces. In 2025, the fee of hiring a non-public license protection legal professional for a Board of Nursing research exceeds $10,000 out of pocket — a price that man or woman malpractice coverage with license safety insurance could deal with entirely.

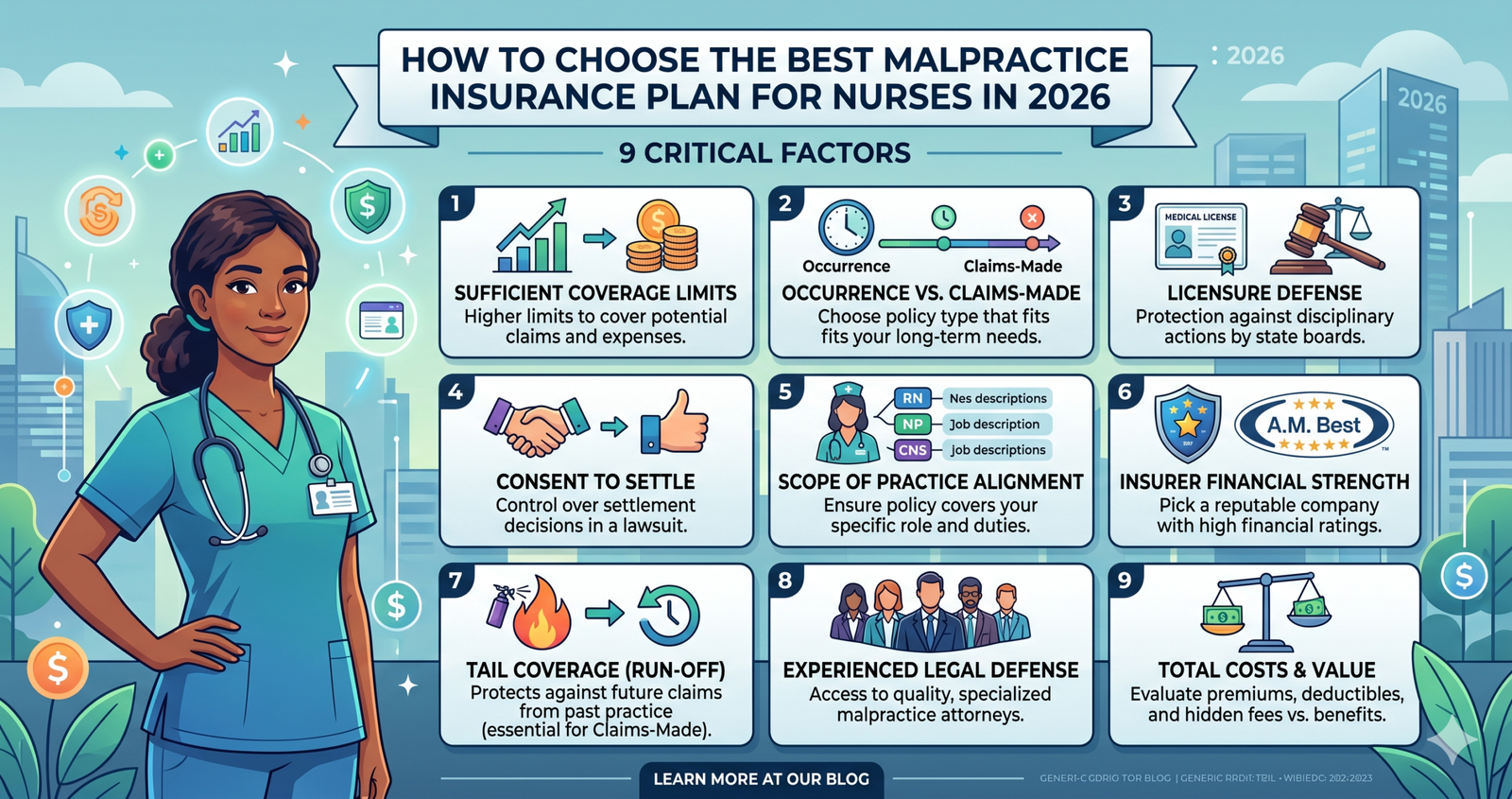

Understanding the 2 Policy Types — Occurrence vs. Claims-Made

The unmarried maximum essential structural choice whilst choosing malpractice coverage is deciding on among an occurrence-primarily based totally coverage and a claims-made coverage. These insurance architectures fluctuate fundamentally, in how and after they defend the nurse, and the monetary outcomes of selecting incorrectly can span a whole career.

An occurrence-primarily based totally coverage covers any incident that takes location at some stage in the lively coverage duration, irrespective of whilst a prison declare is filed — even supposing the declare surfaces years or a long time later, after the coverage has been cancelled or the nurse has retired. This permanent, unconditional safety makes occurrence-primarily based totally insurance broadly seemed because the gold general for long-time period security, specifically in specialties related to pediatrics, wherein statutes of barriers won’t expire till a baby reaches age 18 or 21. Proliability, the handiest AANP-recommended malpractice plan when you consider that 2008, operates completely on an occurrence-primarily based totally version via Liberty Insurance Underwriters.

A claims-made coverage, via way of means of contrast, covers incidents handiest whilst each the occasion and the prison declare are mentioned at the same time as the identical coverage remains lively with the identical insurer. If a nurse adjustments employer, switches insurers, retires, or certainly, we could a claims-made coverage lapse, any destiny claims springing up from that previous insurance duration are left unprotected — except the nurse purchases tail insurance. According to MEDPLI`s 2025 insurance analysis, tail insurance generally prices 200% to 250% of the expiring annual claims-made premium, paid as a one-time lump sum.

For a nurse paying $1,000 in step with 12 months in claims-made premiums, a unmarried activity alternate should cause a $2,000 to $2,500 tail expense. Despite being extra complicated and in the end extra pricey whilst tail prices are factored in, claims-made guidelines are extra not unusual place in employer-backed settings due to the fact they provide decrease preliminary premiums — making them seem cost-powerful with inside the brief time period at the same time as concealing their long-time period monetary exposure.

Factor 1 — Know Your Specialty-Specific Risk Level

Not all nursing roles convey the identical malpractice exposure, and the proper coverage plan ought to mirror the precise scientific surroundings wherein a nurse practices. According to the Nurses Service Organization (NSO) — the nation’s biggest company of nursing legal responsibility coverage — over 80% of all NP malpractice claims stand up inside 4 specialties: number one care, own circle of relatives exercise, behavioral fitness, and gerontology. More than 65% of claims originate in personal doctor practices, personal NP practices, and ageing offerings facilities.

For registered nurses, the highest-chance exercise environments encompass hard work and delivery, the emergency department, ICUs, domestic fitness settings, nursing homes, and business enterprise or in step with-diem roles. In 2025, a developing class of administrative claims has additionally emerged, mainly associated with documentation mistakes in digital fitness records — a chance that cuts throughout all specialties and paintings environments. Nurses in high-acuity specialties or unbiased exercise settings must prioritize better coverage limits and occurrence-primarily based totally insurance, at the same time as the ones in decrease-chance settings may also discover broader flexibility of their insurance choices.

Factor 2 — Evaluate Policy Limits Carefully

Policy limits outline the most monetary safety a malpractice insurer will offer in step with declare and in step with coverage period. The enterprise fashionable for nursing malpractice insurance is $1 million in step with incident and $6 million aggregate — a shape that displays the fact of huge jury awards and multi-declare exposure. For registered nurses, annual charges for $1M/$6M insurance generally variety from $one hundred to $a hundred and sixty in step with year — a remarkably modest funding because the common malpractice payout exceeds $329,000 (thecredentialing.com, 2025).

Nurse practitioners face better top-class tiers of $250 to over $1,500 annually, relying on specialty, exercise setting, and country, due to the fact NPs are often held to the identical fashionable of care as physicians. Nursing college students can stable primary insurance for as little as $35 to $50 in step with year.

When comparing coverage limits, nurses must additionally distinguish between “natural loss” insurance — which covers handiest the quantity provided to the plaintiff — and “closing internet loss” insurance, which additionally consists of legal professional fees, courtroom docket costs, and felony protection prices. The latter affords a long way to go with greater complete monetary safety and must be the baseline fashionable for any expert coverage.

Factor 3 — Confirm License Defense Coverage Is Included

License protection insurance is one of the maximum underappreciated and important additives of any nursing malpractice coverage. While standard malpractice insurance addresses civil proceedings filed with the aid of using patients, license protection insurance affords felony illustration whilst a grievance is filed with the country Board of Nursing — the executive intending that poses the maximum direct chance to a nurse’s cappotential to exercise.

Nurse legal professional Nancy Klein, who taught one of the nation’s first superior NP packages and served as felony problem editor for a main nursing magazine for 25 years, states that maximum states require NPs to hold malpractice coverage and emphasizes that going without it — mainly without license safety — is in no way appropriate below any circumstances.

Sturdy malpractice coverage must additionally encompass repayment for misplaced wages during hearings, insurance for out-of-pocket prices together with journey to proceedings, and private felony illustration this is impartial of any organization or institutional legal professional whose pastimes can also additionally struggle with the nurse’s own.

Factor 4 — Understand the Consent-to-Settle Clause

A regularly not noted however severely essential aspect of malpractice coverage choice is the consent-to-settle provision. This clause determines whether or not a nurse has the criminal proper to refuse a agreement offer — or whether or not the coverage employer can settle a declare at the nurse`s behalf without consent. Settling a declaration, even if its consequences in no formal admission of wrongdoing, can seem with inside the National Practitioner Data Bank (NPDB), an everlasting federal registry that tracks malpractice settlements and unfavorable moves towards healthcare professionals.

NPDB entries can influence clinic credentialing, licensing in different states, employment opportunities, and expert popularity for the rest of a nurse’s career. MedPro Group advises that nurses verify their coverage’s consent provision offers them the specific capacity to refuse agreement — and scrutinize any coverage language that carries hidden exceptions permitting the insurer to settle without the nurse’s expertise or approval.

Factor 5 — Assess Coverage for Telehealth, Volunteering, and Moonlighting

Modern nursing exercise regularly extends past the partitions of a number one business enterprise — via telehealth consultations, moonlighting in pressing care or per-diem roles, nursing domestic volunteer paintings, or worldwide scientific missions. Employer-furnished malpractice insurance nearly uniformly applies handiest to incidents springing up from paintings completed with inside the business enterprise’s institutional setting.

Any scientific interest completed outdoor that setting — inclusive of telehealth care added to sufferers in an exclusive state — can be unprotected below general business enterprise coverage. Personal man or woman malpractice coverage follows the nurse anywhere expert offerings are rendered, making sure non-stop insurance throughout all exercise environments, states, and scientific capacities.

Nurses who paintings in journey nursing, per-diem assignments, or any multi-business enterprise association face mainly acute publicity below claims-made business enterprise guidelines and must prioritize man or woman occurrence-primarily based totally insurance as their number one expert protection.

Factor 6 — Compare Top Providers Before Committing

In 2025, numerous companies stand out as continually encouraged with the aid of using nursing professionals, nurse attorneys, and expert associations. NSO (Nurses Service Organization) is the nation`s biggest devoted nursing legal responsibility insurer, masking all revel in stages from nursing college students via APRNs with their very own unbiased practices, and supplying extra bundled merchandise which includes existence and incapacity insurance. Proliability holds the difference of being the most effective AANP-advocated malpractice plan on account that 2008, working on an occurrence-primarily based totally version with insurance that extends to on-the-job, moonlighting, and volunteer activities.

Berxi, a direct-to-client insurer, lets in nurses to gain fees and buy regulations absolutely online, supplying a mean financial savings of 20% as compared to broker-bought equivalents, with bendy legal responsibility limits up to $1M/$6M. CM&F Group and The Doctors Company have a long time of specialized revel in in healthcare expert legal responsibility and provide sturdy NP-particular regulations with sturdy consent-to-settle provisions. Nurses must gain at minimal 3 aggressive fees, study the great print of every policy’s exclusion carefully, and verify that their nation and area of expertise are blanketed earlier than creating a very last decision.

Factor 7 — Review Coverage Whenever Your Career Changes

Malpractice coverage isn’t always a one-time buy — it’s far a residing issue of expert threat control that need to be actively reviewed at each big profession transition. Leavitt Select Insurance especially advises nurses to check their malpractice insurance on every occasion they alternate employers, transition from hired to unbiased practice, upload a brand-new scientific area of expertise, amplify into telehealth, pass to a brand-new nation, or retirement method.

Each of those transitions can adjust a nurse’s threat profile, render current insurance insufficient, or — with inside the case of claims-made regulations — create risky uninsured gaps to be able to most effectively emerge as obvious years later whilst a declaration subsequently surfaces. Travel nurses and per-diem clinicians, who have alternate employment relationships frequently, are most of the maximum liable to claims-made insurance gaps and must deal with occurrence-primarily based totally character insurance as a non-negotiable profession basis in place of an optionally available supplement.

Conclusion

Choosing the excellent malpractice coverage plan is a number of the maximum consequential expert choices a nurse will make — one which immediately determines the electricity of safety surrounding a profession, a license, and a livelihood. The 2025 proof from NSO, MEDPLI, MedPro Group, Proliability, Berxi, and nurse lawyers practicing in healthcare expert legal responsibility is unambiguous: each nurse wishes person insurance, irrespective of agency coverage.

Understanding the incidence as opposed to claims-made distinction, confirming license protection and consent-to-settle provisions, assessing uniqueness-precise risks, and committing to lively coverage opinions at each profession transition are the pillars of a valid malpractice safety strategy. For nursing college students, RNs, APRNs, nurse educators, and unbiased practitioners alike, the proper malpractice plan is not in reality coverage — it is far from the expert infrastructure that guarantees the liberty to exercise, to grow, and to steer without fear.

FAQs

How tons do malpractice coverage generally price for nurses in 2025?

Registered nurses generally pay among $a hundred and $a hundred and sixty in step with 12 months for $1M/$6M insurance, making it one of the maximum low-priced expert protections available. Nurse practitioners pay greater — among $250 and $1,500 or greater annually — relying on uniqueness and exercise setting. Nursing college students can steady guidelines for as little as $35 to $50 in step with 12 months.

What is the distinction between incidence and claims-made malpractice coverage?

An incidence coverage covers any incident that takes place all through the lively coverage period, irrespective of whilst a declare is later filed — even after the coverage ends. A claims-made coverage simplest covers incidents wherein each the occasion and the prison submitting arise whilst the identical coverage is lively. If claims-made coverage is cancelled, tail insurance should be bought one after the other to preserve safety for beyond incidents.

Does agency-furnished malpractice coverage defend my nursing license?

Generally, no. Employer-furnished malpractice guidelines are written to defend the institution, now no longer the person nurse. They generally exclude Board of Nursing court cases and disciplinary proceedings — the maximum direct and not unusual place danger to a nurse`s license. Individual malpractice coverage with license protection insurance is the simplest way to make sure private prison safety is in administrative hearings.

Do I want malpractice coverage if I am simplest a nursing student?

Yes. NP college students are held responsible to the scope of exercise of a nurse practitioner in scientific settings and may nonetheless be named in a malpractice suit — even if supervised. Many experts’ legal responsibility organizations provide student-precise insurance for as little as $35 to $50 in step with 12 months, and a few NP packages offer fundamental insurance that might not be completely sufficient for all declared types.

Read More:

https://nurseseducator.com/didactic-and-dialectic-teaching-rationale-for-team-based-learning/

https://nurseseducator.com/high-fidelity-simulation-use-in-nursing-education/

First NCLEX Exam Center In Pakistan From Lahore (Mall of Lahore) to the Global Nursing

Categories of Journals: W, X, Y and Z Category Journal In Nursing Education

AI in Healthcare Content Creation: A Double-Edged Sword and Scary

Social Links:

https://www.facebook.com/nurseseducator/

https://www.instagram.com/nurseseducator/

https://www.pinterest.com/NursesEducator/

https://www.linkedin.com/company/nurseseducator/

https://www.linkedin.com/in/afzalaldin/

https://www.researchgate.net/profile/Afza-Lal-Din

https://scholar.google.com/citations?hl=en&user=F0XY9vQAAAAJ