Discover Top 3 Malpractice Insurance Scams Targeting Nurses in 2026: What Every RN Must Know Before Buying Coverage. The pinnacle three malpractice coverage scams concentrated on nurses in 2026. Learn a way to spot faux policies, ghost brokers, and deceptive organization plans earlier than it’s too late.

What Every RN Must Know Before Buying Coverage: Top 3 Malpractice Insurance Scams Targeting Nurses in 2026

Introduction

Malpractice coverage is one of the maximum vital monetary safeguards a nurse can carry. Yet lots of nurses throughout America fall sufferer to coverage fraud every year, frequently without figuring out it till a lawsuit exposes the truth. According to the National Council of State Boards of Nursing (NCSBN) and the American Nurses Association (ANA), expert legal responsibility safety is strongly encouraged for all practicing nurses — making this populace a top goal for scammers. Understanding those threats has in no way been greater pressing in contemporary complicated healthcare landscape.

Why Nurses Are Increasingly Targeted through Malpractice Insurance Scams in 2025

The call for nurse malpractice insurance has risen sharply in current years. The Bureau of Labor Statistics initiatives nursing employment to develop through 6% via 2032, which means greater nurses are actively searching for cheap insurance than ever earlier than. This developing call for creates fertile floor for fraudulent actors who make the most nurses believe, constrained coverage literacy, and choice for low-price premiums.

The upward thrust of virtual marketplaces and social media marketing and marketing has similarly enabled scammers to attain nurses with convincing searching gives that skip conventional vetting processes. Nurses running in high-hazard specialties which include vital care, hard work and delivery, and superior exercise are specifically vulnerable, as their perceived legal responsibility publicity makes them greater motivated — and consequently greater susceptible — to urgency-primarily based totally income tactics.

According to a 2023 record through the Coalition against Insurance Fraud, healthcare specialists together lose masses of hundreds of thousands of greenbacks yearly to cover fraud. Nurses, who frequently buy character insurance independently instead of via institutional HR departments, endure a disproportionate percentage of this hazard.

Insurance student Robert Hunter, former director of coverage on the Consumer Federation of America, has lengthy warned that “affinity fraud” scams concentrated on expert groups — prospers exactly due to the fact sufferers believe that their friends have already vetted the product. For nurses, that belief may be dangerously misplaced.

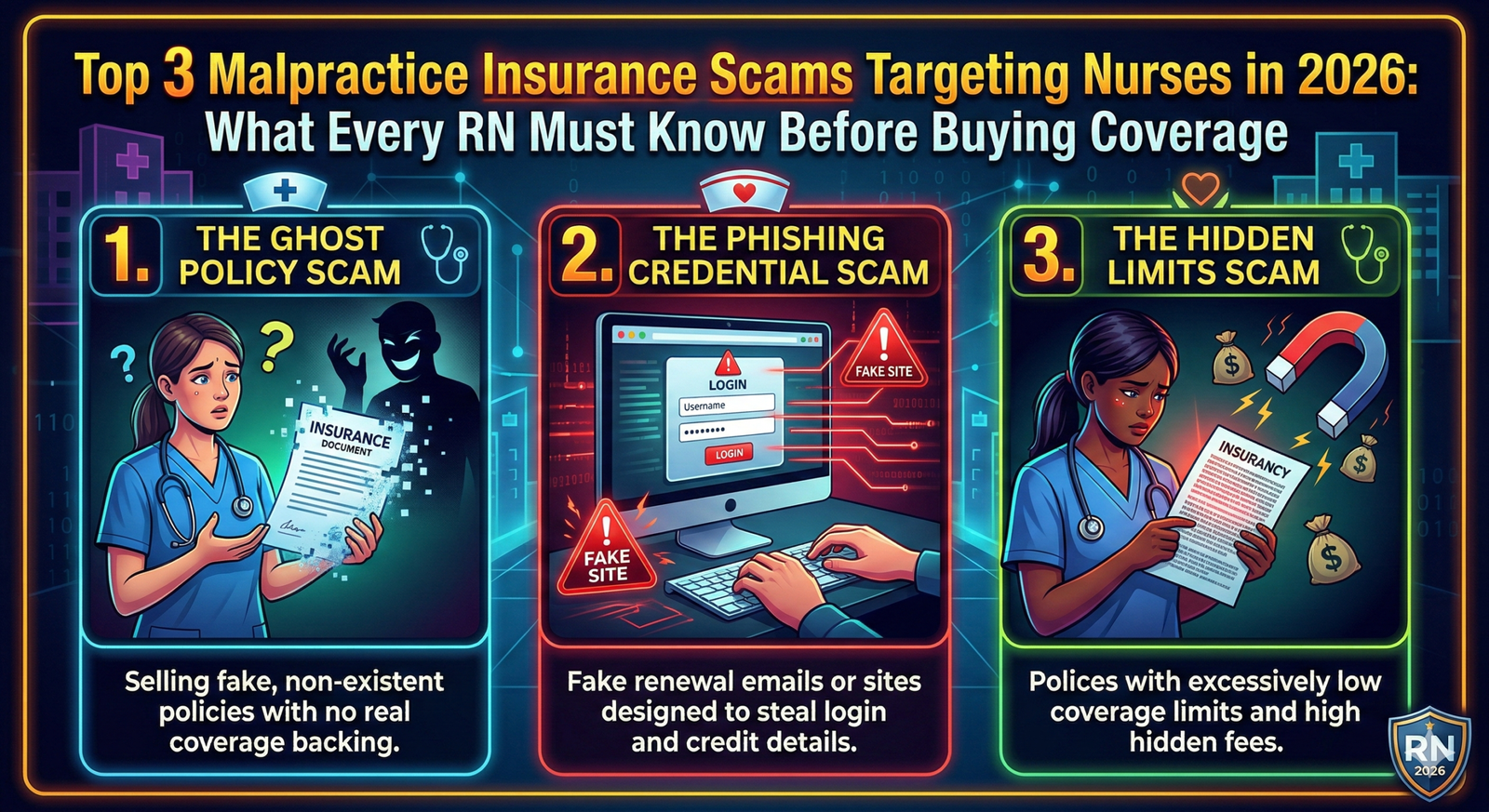

Scam #1 — Fake or Non-Admitted Insurers Posing as Legitimate Carriers

One of the maximum risky and full-size malpractice coverage scams entails fraudulent businesses that pose as certified, valid insurers. These operations construct expert-searching websites, produce polished brochures, or even generate faux coverage files entire with certificates numbers and insurance limits. A nurse can pay her annual top class, get her certificates of coverage, and include it to her employer — by no means understanding that the corporation in the back of it holds no license in her country and has no real claims-paying ability.

Non-admitted insurers are businesses which have no longer been accredited via the means of a country`s Department of Insurance to promote insurance inside that jurisdiction. While a few non-admitted surplus strains companies are valid and function legally beneath unique conditions, fraudulent actors intentionally make the most the complexity of coverage law to confuse buyers. The rip-off commonly unravels while the nurse faces a lawsuit, documents a claim, and discovers the insurer has dissolved, relocated offshore, or become certainly product of the beginning. By that point, she is left protecting a lawsuit without a monetary backing whatsoever.

To guard yourself, continually confirm that any insurer is admitted to your country via means of looking at your country’s Department of Insurance internet site at once. Reputable nurse malpractice companies consisting of NSO (Nurses Service Organization), Proliability via means of Mercer, and CNA Healthcare are well-installed and verifiable. If a corporation does now no longer seems for your country’s certified insurer database, stroll away irrespective of how compelling the fee seems.

Scam #2 — Ghost Policies and Broker-Level Fraud

Ghost coverage fraud is arguably the maximum insidious rip-off concentrated on nurses as it entails a actual human intermediary — a dealer or agent — who seems valid for the duration of the income process. In this scheme, the dealer collects top class payments, troubles faux certificate of coverage bearing the call of an actual or fictitious carrier, and wallet the cash without ever binding real insurance. The nurse walks away believing she is completely protected, whilst the dealer has certainly stolen her top class.

This kind of fraud exploits the agreement with nurse’s region in specialists who seem to function in the industry. The fraudulent dealer may also actually have a functioning internet site, expert email, and social media presence, making detection extraordinarily difficult. In a few documented cases, agents have offered ghost guidelines to dozens of nurses in the identical medical institution system, the use of referrals from unsuspecting colleagues to make rip-off bigger.

The American Association of Nurse Practitioners (AANP) advises all nurses and superior exercise carriers to independently confirm coverage placement at once with the coverage carrier — now no longer simply via the dealer. After shopping for any coverage, name the insurer’s customer support line the use of a range of located on their respectable internet site, offer your call and coverage number, and verify that your insurance is lively and on record. This unmarried verification step can divulge ghost coverage immediately. Never depend totally on certificates of coverage as evidence of insurance.

Scam #3 — Misleading Group Plan Upsells Through Fake or Exploited Associations

The 1/3 most important rip-off objectives nurses via expert affiliation channels — one of the maximum depended on advertising pipelines in nursing. Fraudsters both fabricate nursing institutions completely or accomplice with obscure, loosely regulated agencies to marketplace “exceptional organization malpractice plans” at costs considerably beneath marketplace value. The low rates are the hook; however the excellent print is in which nurses get trapped.

In a lot of those schemes, the coverage exists on paper however carries insurance caps so low — from time to time as little as $25,000 in step with occurrence — that they provide genuinely no real-global safety in a critical malpractice case. Others bring significant exclusion clauses that cast off insurance for the maximum not unusual place styles of nursing legal responsibility claims, such as remedy errors, affected person falls, and documentation failures. Claims-made guidelines offered via those channels often lack tail insurance provisions that mean a nurse who leaves the coverage has no safety for claims filed after her insurance lapses— even for incidents that came about at the same time as she became covered.

The National Nurses United (NNU) and the ANA each warning individuals to scrutinize the legitimacy of any affiliation supplying organization coverage benefits. Before enrolling, independently confirm the affiliation registration and history, request the overall coverage document — now no longer only a summary — and feature the insurance phrases reviewed via way of means of an unbiased coverage marketing consultant or attorney. Policies that cannot resist primary scrutiny have to be suggested on your state’s Department of Insurance.

Conclusion

Malpractice coverage fraud poses a real, growing, and underreported risk to nurses at each level in their careers. Whether the rip-off comes inside the shape of a non-admitted insurer with a resounding website, a ghost broking accumulating rates and not using a purpose of binding insurance, or a deceptive organization plan buried in exclusion clauses, the results for an unprotected nurse dealing with a lawsuit may be financially and professionally catastrophic.

The key takeaways from this dialogue are easy, however vital: confirm each insurer via your state’s Department of Insurance, continually verify your coverage without delay with the carrier, and by no means allow a low top rate to override due diligence. For nursing students, training RNs, superior exercise nurses, educators, and healthcare researchers, expertise those threats isn’t always optional — it’s far an expert responsibility. Protecting your license, your livelihood, and your sufferer’s start off evolved with defensive yourself with legitimate, verifiable insurance from a depended-on provider.

FAQs

FAQ 1: How can I tell if my nurse malpractice insurance policy is legitimate?

Contact your nation`s Department of Insurance to verify the service is certified and admitted to your nation. Then name the insurer at once the use of their authentic internet site variety to confirm your coverage is energetic and on record.

FAQ 2: Are organization malpractice plans via nursing institutions continually secure to purchase?

Not continually. While many association-backed plans are legitimate, a few are tied to fraudulent or difficult to understand organizations. Always confirm the association’s registration, request the entire coverage document, and verify insurance phrases with an impartial marketing consultant earlier than enrolling.

FAQ 3: What have I to do if I suspect I had been offered fraudulent malpractice coverage?

File a criticism right now together along with your nation’s Department of Insurance and phone your nation nursing board. You must additionally seek advice from a certified coverage attorney, mainly in case you are presently going through or awaiting any prison claims in opposition to your practice.

FAQ 4: Is employer-supplied malpractice insurance sufficient for nurses, or do I want my very own coverage?

Employer-supplied insurance usually protects the organization first, now no longer the character nurse. Most nursing organizations, along with the ANA and NCSBN, advise that nurses convey their very own character coverage to make certain non-public safety impartial in their employer’s interests.

Read More:

https://nurseseducator.com/didactic-and-dialectic-teaching-rationale-for-team-based-learning/

https://nurseseducator.com/high-fidelity-simulation-use-in-nursing-education/

First NCLEX Exam Center In Pakistan From Lahore (Mall of Lahore) to the Global Nursing

Categories of Journals: W, X, Y and Z Category Journal In Nursing Education

AI in Healthcare Content Creation: A Double-Edged Sword and Scary

Social Links:

https://www.facebook.com/nurseseducator/

https://www.instagram.com/nurseseducator/

https://www.pinterest.com/NursesEducator/

https://www.linkedin.com/company/nurseseducator/

https://www.linkedin.com/in/afzalaldin/

https://www.researchgate.net/profile/Afza-Lal-Din

https://scholar.google.com/citations?hl=en&user=F0XY9vQAAAAJ