Understand Nurse Practitioner Malpractice Coverage Explained: 7 Critical Facts Every NP Must Know in 2026. Nurse practitioner malpractice insurance in 2025—coverage types, costs, insurance gaps, and why agency coverage on my own is in no way sufficient for NP protection.

7 Critical Facts Every NP Must Know in 2026: Nurse Practitioner Malpractice Coverage Explained

Introduction

Nurse practitioners perform at the vanguard of affected person care; exercise a stage of scientific autonomy that keeps amplifying throughout the United States. With that, increased scope comes a similarly increased prison exposure. According to the 2024 CNA/NSO Nurse Practitioner Professional Liability Exposure Claim Report, the common indemnity fee for NP malpractice claims reached a record $332,137—the very best parent ever documented.

Meanwhile, almost 1/2 of all malpractice charges extended between 2023 and 2024, signaling an unexpectedly tightening legal responsibility landscape. For NPs in any distinctiveness or exercise setting, knowledge malpractice insurance is not optional—it is far an expert and economic imperative.

What Is Nurse Practitioner Malpractice Insurance?

Nurse practitioner malpractice coverage, officially referred to as expert legal responsibility coverage, protects NPs in opposition to claims of negligence or scientific mistakes that bring about affected person harm. Regardless of real fault, a malpractice lawsuit includes amazing economic consequences—consisting of prison protection costs, courtroom docket fees, professional witness expenses, and capacity agreement payouts.

Standard NP malpractice guidelines cowl the value of prison protection, settlements or judgments, licensing board proceedings, and lack of profits for the duration of litigation. The Berxi platform notes that usual legal responsibility limits variety from $500,000 accord to declare with a $1 million aggregate, up to $2 million according to declare with a $6 million aggregate. Selecting the proper insurance ceiling is one of the maximum consequential economic selections an NP will ever make.

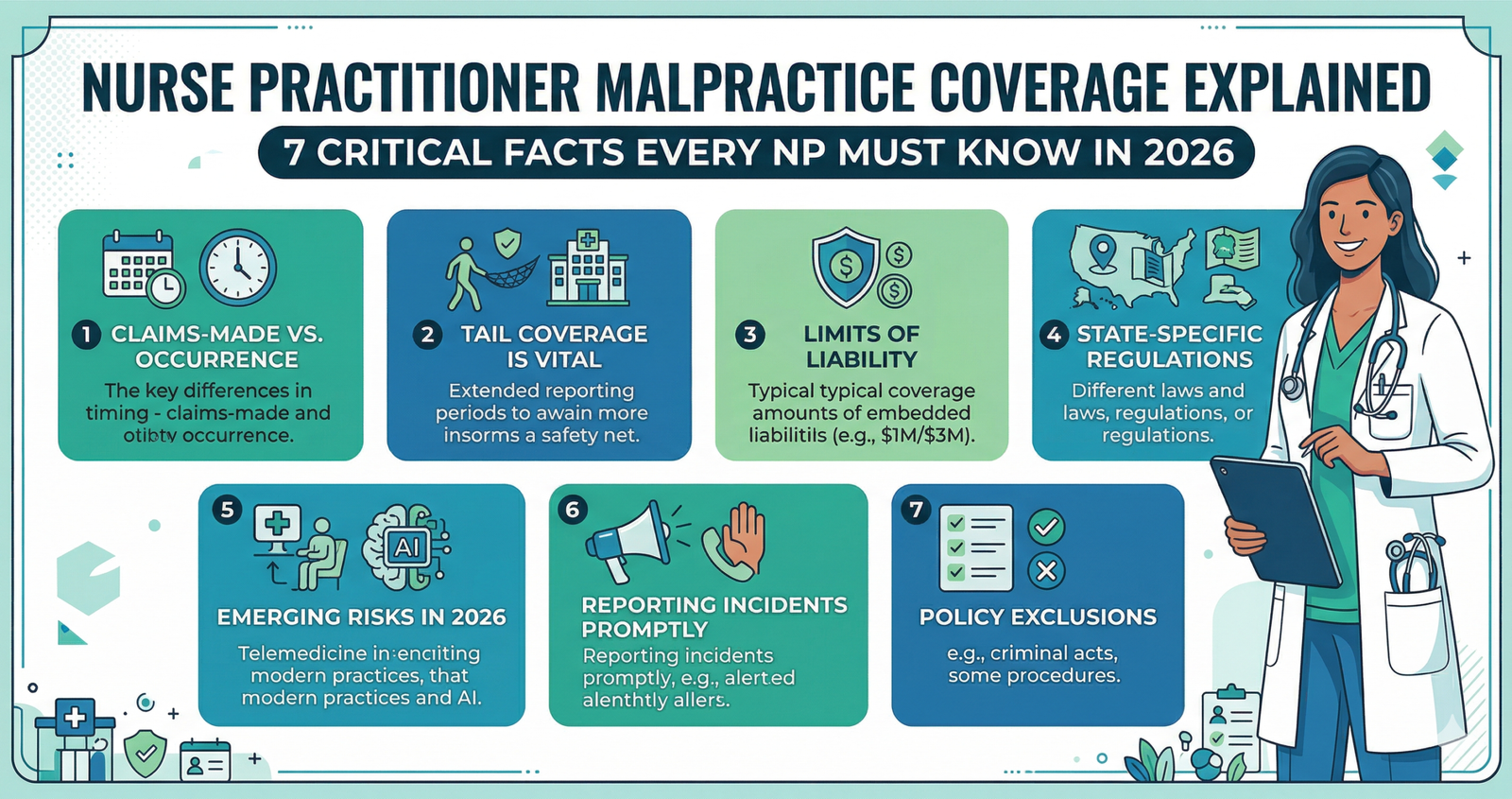

Claims-Made vs. Occurrence Policies: The Critical Difference

Two essentially extraordinary coverage systems exist with inside the NP malpractice market, and complicated them can depart a practitioner financially unprotected. A claims-made coverage most effective offers insurance whilst each the incident and the declare are suggested whilst the coverage stays active. A prevalence coverage, through contrast, covers any incident that takes place throughout the coverage length no matter whilst the declare is sooner or later filed—even years after the coverage has ended.

Occurrence-primarily based totally insurance is broadly taken into consideration the gold trend for long-time period profession safety as it gets rid of the insurance hole that emerges whilst a nurse adjusts employer or leaves a role. Proliability, the most effective AANP-subsidized coverage company considering 2008, gives prevalence-primarily based totally insurance thru Liberty Insurance Underwriters especially for this reason. NPs who deliver claims-made guidelines after which depart a role must purchase “tail insurance” to guard towards behind schedule claims that accumulates appreciably throughout a nursing profession with more than one corporation transition.

Why Employer-Provided Malpractice Insurance Is Often Not Enough

An extensive and financially risky false impression amongst nurse practitioners is that corporation-supplied malpractice coverage gives completely private safety. In reality, corporation guidelines are written in most cases to guard the institution, now no longer the man or woman clinician. The Doctors Company highlights that corporation-supplied insurance regularly leaves essential gaps, such as no safety for Board of Nursing complaints, insufficient man or woman limits whilst guidelines are shared throughout more than one provider, and no insurance for paintings achieved outdoor number one employment together with per-diem shifts, volunteer paintings, or telehealth services.

An unmarried Board of Nursing grievance can take numerous years and lots of bucks to resolve, but maximum corporation guidelines provide zero insurance for this scenario. NPs who additionally paint independently or in more than one care settings face especially acute publicity below corporation-most effective insurance models.

What Does NP Malpractice Insurance Actually Cover?

A well-dependent NP malpractice coverage affords a complete layer of safety that is going a ways past fundamental agreement funding. Coverage normally consists of the whole value of criminal protection—together with lawyer fees, courtroom docket costs, and professional witness fees—frequently out of doors and break free the coverage`s legal responsibility restrict in order that protection prices do now no longer lessen the budget to be had for agreement bills. Most exceptional regulations additionally consist of insurance for licensing board and regulatory proceedings, disciplinary hearings, HIPAA violation protection, and in a few instances, scientific bills to sufferers injured during care.

The Doctors Company’s MediGuard® regulatory danger feature, for example, covers regulatory and license moves up to $25,000 as a integrated element of the malpractice coverage. For NPs serving in scientific director or administrative management roles, supplemental insurance for vicarious legal responsibility—being held liable for mistakes made with the aid of using supervised staff—is a further layer that well-known regulations do now no longer robotically consist of.

How Much Does NP Malpractice Insurance Cost in 2025?

The value of nurse practitioner malpractice coverage varies notably primarily based totally on area of expertise, exercise setting, geographic region, claims records, and coverage type. Proliability reviews rates beginning at $862 yearly for hired grownup NPs and $1,1/2 for self-hired grownup NPs. Berxi locations fashionable NP insurance with inside the variety of $1,500 to over $2,000 in line with year, whilst high-danger specialties consisting of obstetrics, surgery, and neonatal care command substantially better rates reflecting their extended declare frequency.

Geographic region is an effective value motive force as well—NPs working towards in high-litigation states consisting of New York, Pennsylvania, Florida, and Georgia face materially better rates than the ones in states with statutory caps on non-financial damages. California caps non-financial damages at $430,000 for non-wrongful dying instances as of 2025, whilst Texas caps them among $250,000 and $500,000 relying on defendants. Understanding your state’s tort surroundings is an important first step in budgeting for suitable insurance.

Key Factors That Determine Your NP Malpractice Premium

Insurance underwriters examine numerous unique variables whilst calculating an NP’s malpractice premium. Clinical area of expertise is the maximum great factor, as high-acuity regions together with emergency care, exertions and delivery, pediatrics, and vital care deliver statistically better declare costs and agreement values. Prescribing authority additionally affects danger profile—NPs with complete prescriptive authority in complete-exercise-authority states face a broader scope of scientific decision-making and a correspondingly broader legal responsibility exposure.

Personal claims records are reviewed carefully; a smooth report demonstrates decreased danger and normally outcomes in decreased rates over time. The difference among hired and self-hired exercise topics as well, with impartial NPs typically wearing better rates due to the fact they lack any institutional insurance underneath their personal coverage. According to the American Medical Association, almost 1/2 of all malpractice rates rose among 2023 and 2024, making proactive coverage overview an annual expert responsibility.

Top NP Malpractice Insurance Providers to Consider in 2025

Several insurers have established strong reputations for nurse practitioner-specific malpractice coverage. NSO (Nurses Service Organization) is one of the most widely used platforms in the profession, offering tailored NP liability policies with Board of Nursing proceeding coverage included. CM&F Group has a long record of accomplishment of competitive pricing and is recognized for holding inflationary rate increases below market averages over extended periods. Berxi, backed by Berkshire Hathaway Specialty Insurance, provides customizable policies with defense costs fully outside policy limits.

Proliability, as the sole AANP-endorsed provider, is specifically structured around NP professional needs with occurrence-based coverage and straightforward online enrollment. The Doctors Company insures nearly 19,000 NPs nationally, holds an A rating from AM Best, and manages $7.8 billion in assets—financial strength that ensures long-term claims capacity. Comparing quotes across at least two or three of these providers before committing to a policy is the best practice that can yield meaningful premium savings.

Conclusion

Nurse practitioner malpractice insurance is not a bureaucratic checkbox—it is far the economic and expert basis on which a sustainable NP profession is built. With common NP declare indemnity bills achieving a record $332,137 in 2024, and felony protection expenses mechanically exceeding $50,000 to $100,000 even in instances in which no negligence is in the end found, the stakes of being underinsured are profound. The key takeaways from this manual are clear: occurrence-primarily based totally rules provide advanced long-time period safety over claims-made structures, company insurance nearly continually leaves important non-public gaps, and specialty, location, and claims record every drastically form your premium.

Whether you are a newly certified NP getting into your first position, a skilled practitioner transitioning to unbiased practice, a nursing educator guiding the following generation, or a nurse researcher advising on expert standards, securing committed man or woman malpractice insurance is the various maximum critical profession selections you will make. Review your coverage annually, evaluate carriers actively, and in no way permit insurance gaps to head unaddressed.

FAQs

Do nurse practitioners want their personal malpractice coverage if their company already offers insurance?

Yes. Employer-furnished rules are designed to guard the institution, now no longer the man or woman NP. They normally exclude Board of Nursing complaints, off-web website online paintings, and consistent with-diem assignments—gaps that non-public malpractice insurance is specially designed to fill.

What is tail insurance, and while does an NP want it?

Tail insurance is a coverage extension that protects against claims filed after claims made coverage has ended. NPs want it each time they depart a position, extrade employers, or retire whilst protecting a lively claims-made coverage to keep away from being uncovered to not on time complaints from beyond affected person care.

How lot malpractice insurance does a nurse practitioner without a doubt want?

Most NP rules offer a minimal of $1 million consistent with declaration and $three million aggregates, although high-threat specialties or unbiased practitioners regularly require better limits. Reviewing your state`s felony surroundings and consulting with a healthcare legal responsibility professional facilitates decide the proper insurance ceiling on your practice.

Does NP malpractice coverage cowl telehealth and consistent with-diem nursing paintings?

Individual non-public malpractice rules normally amplify insurance to all expert activities, consisting of telehealth consultations and consistent with-diem assignments. Employer-furnished rules commonly do now no longer cowl paintings executed out of doors of the number one employment setting, making non-public insurance critical for NPs running in a couple of environments.

Read More:

https://nurseseducator.com/didactic-and-dialectic-teaching-rationale-for-team-based-learning/

https://nurseseducator.com/high-fidelity-simulation-use-in-nursing-education/

First NCLEX Exam Center In Pakistan From Lahore (Mall of Lahore) to the Global Nursing

Categories of Journals: W, X, Y and Z Category Journal In Nursing Education

AI in Healthcare Content Creation: A Double-Edged Sword and Scary

Social Links:

https://www.facebook.com/nurseseducator/

https://www.instagram.com/nurseseducator/

https://www.pinterest.com/NursesEducator/

https://www.linkedin.com/company/nurseseducator/

https://www.linkedin.com/in/afzalaldin/

https://www.researchgate.net/profile/Afza-Lal-Din

https://scholar.google.com/citations?hl=en&user=F0XY9vQAAAAJ