Understand Claims-Made vs Occurrence Malpractice Insurance Policies Explained: A 2026 Guide Every Nurse Must Read. Claims-made vs. prevalence malpractice coverage rules in 2025. This nurse`s manual explains insurance, tail coverage, charges, and which coverage pleasant protects your license.

Claims-Made vs Occurrence Malpractice Insurance Policies Explained: A 2026 Guide Every Nurse Must Read

Introduction

Nursing malpractice coverage is now no longer optional — it’s far an essential act of expert self-safety in 2025. According to a 2024 evaluation with the aid of using Claggett, Sykes & Garza Trial Lawyers, 12,655 registered nurses have been named in malpractice claims in 2024 alone, surpassing physicians for the primary time in recorded history. With common malpractice agreement payouts nationally reaching $427,443 in 2024, and man or woman felony protection charges robotically exceeding $50,000 to $100,000 even if no negligence is in the end found, the stakes have in no way been higher.

Yet regardless of this reality, a placing range of nurses — each beginner and experienced — do now no longer absolutely recognize the unmarried maximum consequential selection inside their malpractice insurance: whether they maintain a claims-made coverage or a prevalence coverage. This manual explains each clearly, comparatively, and practically, in order that each nurse could make an informed, career-shielding choice.

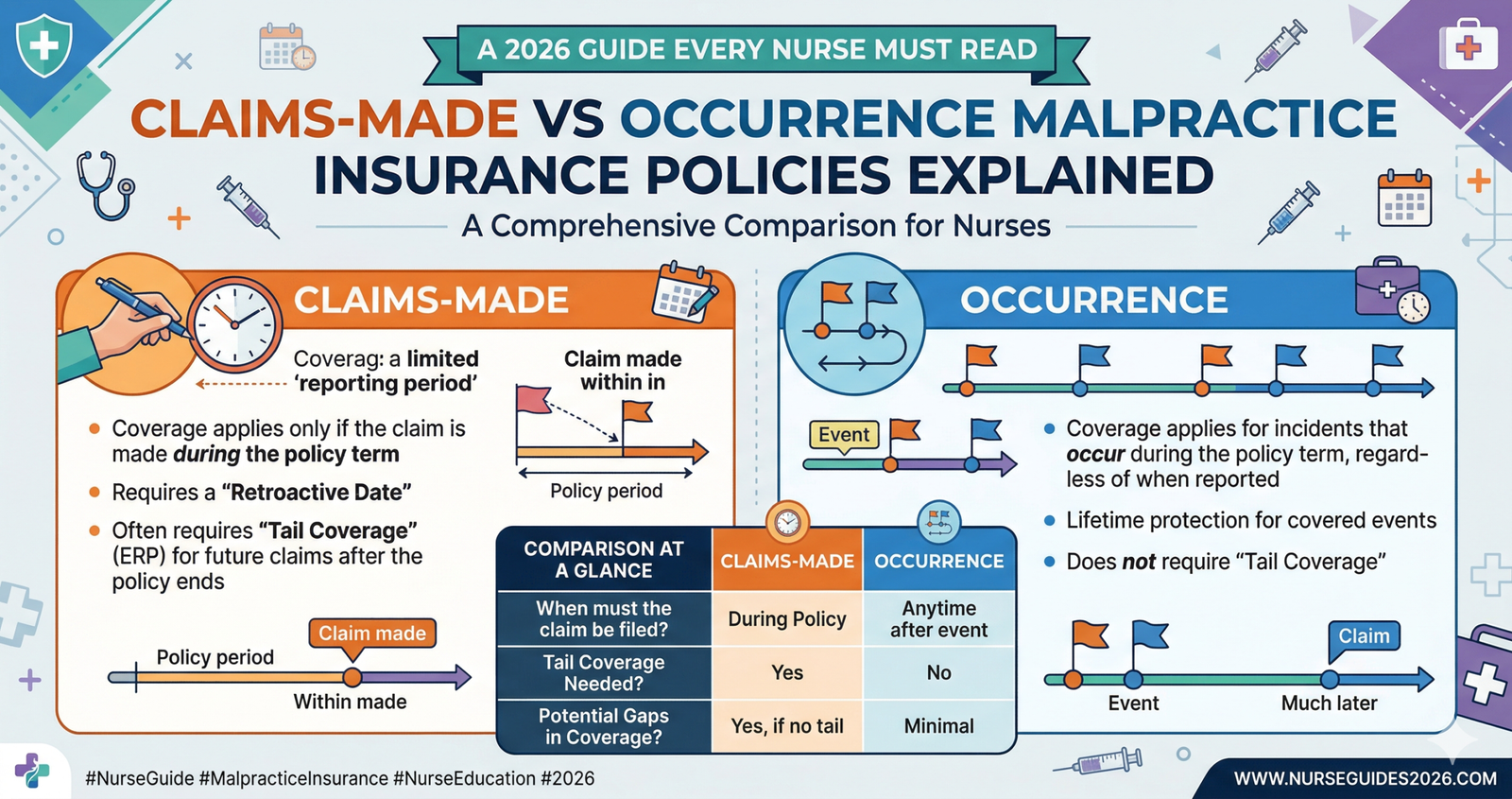

The Core Distinction: How Coverage Is Triggered

The maximum vital distinction among claim-made and prevalence rules lies in a unmarried question: does insurance activate? Understanding this difference isn’t always a technicality — it’s far the distinction between being absolutely covered and coming across a catastrophic insurance hole exactly whilst you want safety maximum.

A prevalence coverage covers any incident that takes vicinity at the same time as the coverage is energetic, irrespective of while the ensuing declaration is finally filed. As Nancy J. Brent, MS, JD, RN — a nurse legal professional and creator of the textbook Nurses and the Law — explains, with a prevalence coverage, if the incident occurred throughout your insurance period, you’re covered even supposing the declare surfaces years or a long time later. This feature makes prevalence rules broadly seemed because the gold popular of nursing malpractice insurance. They are analogous to house owners or car legal responsibility coverage: insurance follows the event, now no longer the office works timeline.

Claims-made coverage, with the aid of using contrast, covers a declaration handiest while each the incident and the formal submitting of the declaration arise at the same time as the coverage is energetic with the equal insurer. If you dealt with a affected person in 2022 beneath service A’s claims-made coverage, then switched to service B in 2023, and that affected person documents a grievance in 2025 — you aren’t included beneath both coverage until you took deliberate, extra steps to defend yourself. This structural quandary is the defining vulnerability of claims-made insurance, and it’s far one which each nurse ought to recognize earlier than signing any coverage agreement.

What Is Tail Coverage and Why Does It Matter?

Tail insurance — officially referred to as a prolonged reporting endorsement — is the bridge that closes the space left with the aid of using claims-made coverage whilst it ends. When a nurse leaves a process, retires, modifications states, or switches coverage carriers, their claims-made coverage stops protecting them in the interim the coverage terminates. Any declaration filed after that point — even for an incident that took place years in advance, all through lively insurance — can be denied without tail coverage in place.

The price of tail insurance is substantial and ought to be factored into any sincere assessment of the 2 coverage sorts. According to MEDPLI`s 2025 coverage analysis, tail coverage commonly expenses two hundred to 250 percentage of the expiring claims-made annual top class, paid as a one-time lump sum. This manner a nurse paying $500 according to 12 months beneath a claims-made coverage should face a $1,000 to $1,250 tail charge whenever they alternate employers or permit their coverage to lapse. Over a 30-12 months nursing profession with more than one process modification, the cumulative price of tail insurance can without difficulty rival or exceed the whole price of a prevalence coverage — a truth this is regularly disregarded whilst nurses first evaluate top class prices.

The statute of barriers problem deepens this undertaking considerably. As lawyer Nancy Brent notes, pediatric nursing claims are in particular vulnerable: the statute of barriers for alleged accidents to a minor does now no longer start walking till the kid turns 18, and in a few states, extends to age 21. A nurse who labored in pediatrics beneath a claims-made coverage without preserving non-stop insurance — or without shopping tail insurance — should face a declaration two decades after the incident and not use a safety coverage whatsoever.

A Side-with the aid of using-Side Cost Comparison

Nurses comparing those coverage sorts ought to appearance past the preliminary top class to recognize the complete, lifetime price of every option. The price systems are basically different, and neither kind is universally less expensive whilst regarded over a complete professional timeline.

Occurrence guidelines bring better in advance rates due to the fact the insurer ought to charge the coverage to account for an open-ended claims window — they may be assuming threat for claims that can be filed 5, 10, or maybe two decades with inside the future. According to present day 2025 marketplace data, RN prevalence-primarily based totally man or woman guidelines from vendors together with CM&F Group begin at approximately $113 according to 12 months for $1 million in insurance, making them remarkably low priced relative to the safety they provide. Nurse Practitioner quotes beneath prevalence guidelines variety from $250 to over $1,500 annually, relying on area of expertise and exercise setting, reflecting the elevated scope of NP exercise and correspondingly better common declare values.

Claims-made regulations start with decrease preliminary rates — an appealing characteristic for brand spanking new graduates dealing with budget carefully — however prices growth appreciably every 12 months because the coverage matures. As MEDPLI`s evaluation confirms, rates generally double from 12 months one to 12 months and keep growing till the coverage absolutely matures at about 4 to 5 years. The insurer can alter prices yearly below a claims-made structure, making long-time period price prediction greater difficult. When tail insurance charges are introduced at the stop of the coverage, the whole expenditure often surpasses what prevalent coverage could have price over the identical period.

Employer Coverage: Why It Is Never Enough on Its Own

One of the maximum chronic and professionally risky misconceptions in nursing is the notion that business enterprise-supplied malpractice coverage makes character insurance unnecessary. This false impression leaves nurses uncovered in as a minimum 3 important approaches that no business enterprise coverage can address.

First, the business enterprise’s coverage business enterprise represents the institution — now no longer the character nurse. When each clinic and a nurse are named in a lawsuit, the institutional insurer may also pursue a decision that protects the facility’s pastimes even if doing so harms the nurse’s expert record. Private coverage ensures criminal illustration, this is solely devoted to protecting the nurse’s license, income, and reputation.

Second, business enterprise-supplied insurance nearly universally excludes Board of Nursing court cases and disciplinary proceedings — the maximum common criminal threats nurses simply face. In 2025, hiring a personal license protection legal professional for a Board of Nursing research charges upward of $10,000 out of pocket; character coverage with license safety insurance transforms that disaster right into a controlled process.

Third, business enterprise regulations are claims made through default in almost all healthcare employment settings. When a nurse modifications jobs, that insurance ends immediately — leaving any incident from their preceding employment probably unprotected until they negotiate and pay for tail insurance, which employers aren’t obligated to provide.

Choosing the Right Policy: Key Decision Factors for Nurses

The proper malpractice coverage for any character nurse relies upon on a cautious evaluation in their scientific specialty, profession stage, employment situation, and state-particular threat profile. Several choice elements stand out as specifically crucial in 2025.

Nurses run in high-acuity specialties — which include in depth care, emergency nursing, exertions and delivery, pediatrics, and superior exercise roles — convey statistically better malpractice threat and commonly advantage maximum from the permanent, unconditional insurance that a prevalence coverage provides. The 2024 CNA/NSO Nurse Practitioner Professional Liability Exposure Claim Report showed that the common indemnity fee for NP claims reached a record $332,137, underlining the want for robust, long-time period insurance architecture.

Nurses in journey or in line with diem roles, who often extrade employers and coverage carriers, face specifically acute tail insurance demanding situations below claims-made systems and must strongly not forget character prevalence-primarily based totally regulations as a strong basis no matter something business enterprise insurance they receive.

For nurses who presently preserve claims-made rules, the realistic precedence is making sure that tail insurance is negotiated earlier than any task change, retirement, or coverage transfer takes effect. As Jennifer Flynn, Vice President of Risk Management at NSO inside Aon`s Affinity Insurance Services — with over 24 years of healthcare coverage experience — advises: “When you purchase the tail, that brings your insurance thru but a few years you purchase the tail for.” Requesting that a departing business enterprise cowl the value of tail coverage as a part of an employment transition is a negotiable and professionally suitable ask that many nurses do no longer realize to make.

Conclusion

Understanding the distinction among claims-made and prevalence malpractice coverage rules isn’t always a felony formality — it’s miles a profession-defining choice that each nurse, nurse practitioner, educator, and nursing pupil need to make with complete statistics and clean expert intent. Occurrence rules provide everlasting, unconditional safety that follows the incident as opposed to the office work timeline, making them the gold general for long-time period profession security. Claims-made rules provide decrease preliminary charges however introduce significant insurance gaps that require tail coverage to close — a value that accumulates notably throughout a nursing profession with a couple of business enterprise transitions.

In a panorama in which 12,655 registered nurses confronted malpractice claims in 2024 alone, in which common agreement payouts exceed $427,000, and in which Board of Nursing lawsuits are developing yr over yr, no nurse can manage to pay for to make this choice via way of means of default. For nursing college students coming into the profession, training nurses at each profession stage, and nursing educators liable for getting ready the subsequent technology of clinicians, this understanding isn’t always optional — it’s miles foundational expert literacy.

FAQs

What is the primary distinction among claims-made and a prevalence malpractice coverage for nurses?

A claims-made coverage handiest covers you if each the incident and the formal declare are filed even as the identical coverage is active, that means insurance ends whilst the coverage ends. A prevalence coverage covers any incident that passed off throughout the coverage length no matter whilst the declaration is later filed, supplying everlasting safety without the want for tail coverage.

Is tail coverage always necessary when a claims-made policy ends?

Yes — in case you maintain a claims-made coverage and extrade employers, retire, or transfer insurers without buying tail insurance, any declare filed after your coverage ends will now no longer be included even though the incident took place at some point of your energetic insurance period. Tail insurance normally fees two hundred to 250 percent of your annual claims-made top class and is a one-time buy at coverage termination.

Why do maximum nurses acquire claims-made rules from their employers in preference to prevalence rules?

Employers and insurers decide upon claims-made rules due to the fact the finite insurance window lets in rates to be adjusted annually, giving insurers more manage over their threat exposure. This association financially favors the organization however locations the weight of tail insurance — and the related cost — at the man or woman nurse at each profession transition.

Do nurses who’re included through their company`s malpractice coverage nonetheless want their personal man or woman insurance?

Strongly yes. Employers rules are designed to shield the organization first, nearly in no way cowl Board of Nursing proceedings or license protection proceedings, and terminate at once while employment ends. A man or woman coverage guarantees a devoted prison advocate, license safety insurance, and uninterrupted safety that travels with the nurse no matter company or area changes.

Read More:

https://nurseseducator.com/didactic-and-dialectic-teaching-rationale-for-team-based-learning/

https://nurseseducator.com/high-fidelity-simulation-use-in-nursing-education/

First NCLEX Exam Center In Pakistan From Lahore (Mall of Lahore) to the Global Nursing

Categories of Journals: W, X, Y and Z Category Journal In Nursing Education

AI in Healthcare Content Creation: A Double-Edged Sword and Scary

Social Links:

https://www.facebook.com/nurseseducator/

https://www.instagram.com/nurseseducator/

https://www.pinterest.com/NursesEducator/

https://www.linkedin.com/company/nurseseducator/

https://www.linkedin.com/in/afzalaldin/

https://www.researchgate.net/profile/Afza-Lal-Din

https://scholar.google.com/citations?hl=en&user=F0XY9vQAAAAJ