Learn Understanding Claims-Made vs Occurrence Policies: 7 Key Differences Every Nurse Must Know in 2026. The important variations among claims-made and incidence malpractice regulations for nurses. Discover which insurance kind protects your nursing profession quality in 2026.

7 Key Differences Every Nurse Must Know in 2026: Understanding Claims-Made vs Occurrence Policies

Introduction

Professional legal responsibility coverage represents an essential safety mechanism for nurses navigating today`s complicated healthcare surroundings in which malpractice claims hold growing steadily. According to the American Nurses Association (ANA) Risk Management Database, about 1 in 10 nurses will face a malpractice declare throughout their profession, with common agreement charges exceeding $250,000 as of 2025?

Understanding the differences among claims-made and incidence-primarily based totally malpractice regulations proves critical for securing good enough expert safety. The National Council of State Boards of Nursing emphasizes that many nurses stay ignorant of important insurance gaps that emerge from coverage kind misunderstandings, doubtlessly exposing them to devastating economic legal responsibility.

Recent statistics from the Nurses Service Organization show that coverage choice mistakes contribute to about 30 percentages of insurance denials, underscoring the significance of knowledgeable decision-making concerning expert legal responsibility shape and timing.

Defining Claims-Made Malpractice Insurance Policies

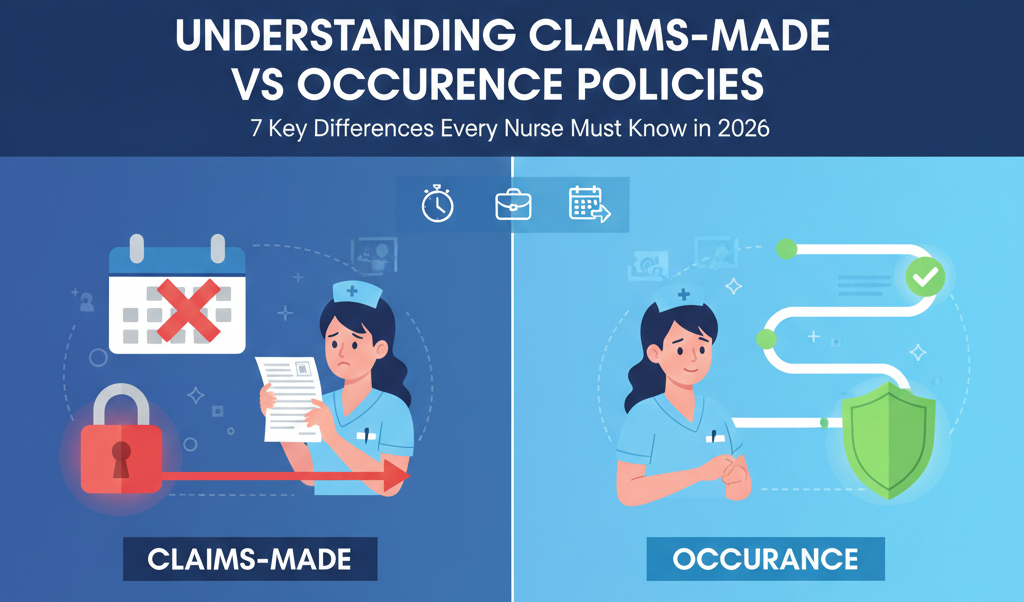

Claims-made regulations offer insurance completely for incidents that each arise and are stated throughout the energetic coverage period. This temporal limit creates a completely unique insurance shape in which the coverage need to stay energetic while the declare is filed, no matter while the alleged negligent act occurred. According to Nurse’s Legal Handbook, sixth Edition (2020), claims-made regulations function on a dual-cause machine requiring each the incident and the declare reporting to fall inside specific timeframes for insurance activation.

The retroactive date represents an important thing of claims-made regulations, setting up the earliest date for which incidents can be blanketed beneath the cutting-edge coverage. When nurses buy their first claims-made coverage, the retroactive date usually corresponds with the coverage powerful date, developing instant insurance for destiny incidents. Understanding this retroactive date proves critical due to the fact any alleged negligence going on earlier than this date falls outdoor insurance parameters no matter while the declaration is stated.

Premium systems for claims-made regulations show step-up styles throughout preliminary coverage years. The Insurance Information Institute reviews that 1-12 months claims-made rates usually price 50-60 percentage much less than mature coverage rates, with systematic increase going on yearly till achieving complete adulthood round 12 months five. This graduated pricing displays the increasing insurance window as regulations age, masking an increasingly extensive time frame of capability incidents as every 12 months passes and the retroactive date stays fixed.

Claims-made regulations require cautious attention throughout professional transitions consisting of retirement, employment changes, or shifts among exercise settings. The Nursing Economics journal (2024) highlights that nurses who cancel claims-made regulations without securing tail insurance create everlasting gaps in expert legal responsibility safety for all incidents going on throughout the cancelled coverage period. These insurance gaps persist indefinitely, exposing nurses to full-size economic threat even many years after leaving scientific exercise if claims emerge from ancient, affected person care encounters.

Understanding Occurrence-Based Malpractice Coverage

Occurrence guidelines offer everlasting insurance for any incident taking place for the duration of the coverage duration, no matter whilst claims are in the end reported. This insurance shape removes worries approximately timing of declare reporting, supplying long-time period safety that persists even after coverage cancellation or retirement from nursing exercise. According to the American Association of Nurse Attorneys, prevalence-primarily based totally guidelines perform on a single-cause device wherein best the incident timing subjects for insurance determination, now no longer the declare reporting date.

The everlasting nature of prevalence insurance creates massive benefits for nurse’s worried approximately prolonged statute of barriers durations or behind schedule declare discoveries. Medical malpractice claims might also additionally emerge years or maybe many years after alleged incidents, especially in instances regarding minors wherein statutes of barriers regularly increase till the affected person reaches maturity plus extra years. Research posted with inside the Journal of Nursing Regulation (2025) documented instances wherein malpractice claims surfaced extra than twenty years post-incident, emphasizing the price of prevalence-primarily based totally guidelines` enduring safety.

Premium systems for prevalence guidelines exhibit flat pricing styles reflecting complete insurance from coverage inception. Unlike claims-made step-up pricing, prevalence rates continue to be exceptionally solid yr-to-yr, although they normally price 40-60 percentages extra to begin with than first-yr claims-made rates in line with coverage enterprise analyses. This better in advance price represents fee for everlasting insurance that removes destiny tail insurance costs and offers peace of thought concerning indefinite safety.

Occurrence guidelines especially advantage nurses looking forward to profession changes, retirement planning, or common employment transitions. The Agency for Healthcare Research and Quality note that common nursing careers contain more than one organization, exercise placing shifts, and ability durations of medical inactivity. Occurrence-primarily based totally insurance contains those profession styles seamlessly, retaining safety throughout all transitions without requiring extra tail insurance purchases or coverage continuity protection that claims-made systems demand.

Tail Coverage: Bridging the Claims-Made Coverage Gap

Extended reporting endorsements, normally termed tail insurance, constitute supplemental coverage buying everlasting claims-made insurance extension after coverage termination. Tail insurance converts the time-restrained nature of claims-made guidelines into everlasting safety mirroring prevalence-primarily based totally insurance for the precise coverage duration being prolonged. According to NSO Risk Advisor guidance (2025), tail insurance purchases show critical for nurses retiring, converting insurers, or leaving exercise settings wherein organization-supplied claims-made insurance terminates.

The economic funding required for tail insurance represents an enormous amount of attention in coverage choice decisions. Industry requirements imply tail insurance generally charges 150-three hundred percent of the very last annual top rate, developing a tremendous one-time price at profession end or employment transition points. For example, a nurse paying $500 yearly for mature claims-made insurance may face tail insurance charges ranging from $750 to $1,500 to steady everlasting safety for that coverage duration.

Alternatives to conventional tail insurance consist of nostril insurance or previous acts insurance presented with the aid of using a few insurers whilst nurses transfer among claims-made rules. Nose insurance extends the brand-new coverage`s retroactive date backward, protecting incidents from preceding employment or coverage durations. The American Nurses Association recommends cautiously comparing whether new employers or coverage providers provide unfastened or discounted nostril insurance as this notably reduces the economic burden of keeping non-stop safety throughout coverage transitions.

Strategic timing of tail insurance purchases affects each price and insurance adequacy. Purchasing tail insurance straight away upon coverage termination guarantees no gaps in safety, although a few providers provide prolonged buy home windows permitting not on time decisions. However, the Journal of Healthcare Risk Management (2024) cautions that delaying tail insurance purchases creates durations of vulnerability in which claims suggested at some stage in the space duration may also fall outdoor any insurance parameters, exposing nurses to finish economic obligation for protection charges and ability settlements.

Comparing Premium Costs: Long-Term Financial Implications

Understanding the whole lifetime price of expert legal responsibility coverage calls for studying each preliminary top rate costs and ability tail insurance obligations. Claims-made rules gift decrease access charges however necessitate eventual tail insurance purchases to keep everlasting safety. According to actuarial analyses posted with the aid of using the National Association of Insurance Commissioners, nurses keeping claims-made insurance at some point of 30-12 months careers and shopping tail insurance at retirement generally pay 15-25 percentage less in general charges in comparison to prevalence insurance over same timeframes.

However, person profession trajectories notably affect which coverage kind gives advanced economic value. Nurses experiencing common activity changes, brief exercise interruptions, or more than one company transitions frequently incur repeated tail insurance costs with claims-made rules. Research from Nursing Management journal (2025) demonstrates that nurses converting employers for extra than 4 instances throughout their careers often pay extra in cumulative charges and tail insurance charges with claims-made systems in comparison to keeping non-stop prevalence-primarily based totally insurance.

Budget predictability represents every other monetary attention distinguishing those coverage types. Occurrence charges continue to be surprisingly strong and predictable throughout profession spans, facilitating long-time period monetary making plans and budgeting. Conversely, claims-made charges boom systematically in preliminary years earlier than stabilizing, and the eventual tail insurance requirement creates a significant, lump-sum price at profession end that nurses must assume and price range for years in advance.

Employer-furnished expert legal responsibility coverage complicates fee comparisons because many healthcare centers provide claims-made insurance without rate to hired nurses. The American Organization for Nursing Leadership reviews that about 70 percentages of hospital-hired nurses get hold of organization-paid expert legal responsibility insurance, although maximum guidelines terminate straight away upon employment end. Nurses depending solely on organization insurance must understand the tail insurance responsibility they inherit whilst leaving employment, doubtlessly dealing with sudden charges of numerous thousand bucks to hold safety for his or her employment period.

Coverage Gaps and Protection Risks

Lapses in expert legal responsibility insurance create vulnerability home windows exposing nurses to catastrophic monetary effects if malpractice claims emerge from unprotected periods. Claims-made guidelines exhibit precise susceptibility to insurance gaps in the course of employment transitions, coverage provider changes, or brief exercise interruptions. According to danger control records from CNA HealthPro, about forty percent of nurses revel in insurance gaps exceeding 30 days in some unspecified time in the future during their careers, frequently unknowingly developing everlasting uninsured publicity periods.

The mechanisms developing insurance gaps vary essentially among coverage types. Occurrence insurance gaps emerge best whilst nurses exercise with nonenergetic coverage, a surprisingly truthful situation commonly attributable to aware choices to forego insurance or brief exercise cessations among securing new guidelines. Claims-made gaps show greater complex, bobbing up now no longer best from practicing without energetic guidelines however additionally from retroactive date misalignments, cancelled guidelines without tail insurance, and not on time declare reporting past coverage periods.

Statute of obstacles versions throughout states and affected person populations compound insurance whole dangers. While maximum states impose scientific malpractice declaring closing dates starting from to 6 years post-incident, exceptions exist for instances regarding minors, fraudulent concealment, or overseas item retention. The Journal of Nursing Law (2024) documented instances in which claims emerged 15-two decades post-incident, emphasizing that even decades-vintage insurance gaps hold ability for devastating monetary publicity if claims floor from unprotected exercise periods.

Mitigating insurance whole dangers calls for meticulous interest to cover continuity, retroactive date alignment, and tail insurance procurement. The National Nurses in Business Association recommends keeping particular facts of all expert legal responsibility guidelines which include powerful dates, retroactive dates, insurance limits, and tail insurance purchases. This documentation proves important for verifying non-stop insurance if claims emerge years after alleged incidents, specifically because coverage provider facts might also additionally emerge as inaccessible over prolonged timeframes because of mergers, acquisitions, or enterprise closures.

Policy Selection Factors: Matching Coverage to Career Stage

Early-profession nurses regularly advantage from claims-made rules` decrease preliminary charges, making expert legal responsibility coverage extra financially on hand at some point of years while scholar mortgage duties and entry-degree salaries constrain budgets. According to the National Student Nurses Association (2025), about sixty five percentage of newly graduated nurses deliver scholar mortgage debt averaging $40,000, making fee issues mainly applicable for starting practitioners. The graduated top-class shape of claims-made rules aligns properly with regular professional income trajectories wherein salaries growth significantly at some point of preliminary exercises years.

Mid-profession nurses deliberating unique transitions, superior exercise education, or geographic relocations should cautiously examine how coverage kinds accommodate expected modifications. Claims-made rules require tail insurance purchases or nostril insurance preparations with every substantial transition, growing administrative complexity and capacity expense. Conversely, prevalence insurance continues seamless safety throughout all profession modifications without requiring extra insurance purchases or coverage coordination among antique and new coverage preparations.

Nurses drawing near retirement face wonderful insurance issues prioritizing long-time period safety without ongoing top-class duties. Occurrence rules bought at some point of very last operating years offer everlasting insurance without tail costs, although better annual charges can also additionally appear much less appealing while profession period last is limited. The American Nurses Association Retirement Planning Guide indicates that nurses inside 5 years of retirement regularly locate prevalence insurance extra fee-powerful while general costs consisting of tail insurance are calculated, despite better annual charges at some point of operating years.

Part-time nurses, in keeping with Diem staff, and nurses with intermittent exercise styles, come across insurance demanding situations irrespective of coverage kind selected. Claims-made rules require non-stop preservation even at some point of non-exercise durations to keep retroactive dates, growing ongoing costs at some point of earnings interruptions. Occurrence rules get rid of this difficulty via means of imparting everlasting insurance for exercise durations irrespective of next profession interruptions; although nurses should make sure lively insurance exists at some point of all real exercise durations to keep away from uninsured publicity at some point of scientific work.

Regulatory Requirements and Professional Standards

State nursing board guidelines not often mandate expert legal responsibility coverage as licensure necessities, although a few states require nurses to reveal insurance fame to employers or patients. According to the National Council of State Boards of Nursing 2025 survey, handiest 4 states impose direct expert legal responsibility coverage necessities for nursing licensure, although many states inspire or advise insurance thru exercise act language or regulatory guidance. Understanding precise kingdom necessities proves crucial for making sure regulatory compliance along ok expert safety.

Advanced exercise registered nurses face extra stringent coverage necessities as compared to registered nurses, mainly concerning prescriptive authority and impartial exercise privileges. Medicare situations of participation, much kingdom scope of exercise laws, and clinic credentialing requirements regularly mandate precise expert legal responsibility insurance limits for nurse practitioners, scientific nurse specialists, and licensed nurse midwives. The American Association of Nurse Practitioners reviews that minimal required insurance limits generally variety from $1 million in keeping with prevalence and $three million aggregates, although a few exercise settings call for better limits.

Professional company requirements and function statements offer steerage concerning suitable legal responsibility insurance even absent regulatory mandates. The American Nurses Association Code of Ethics Provision five emphasizes nurses` responsibility to guard themselves, patients, and co-workers through preserving competence and securing ok expert protections such as legal responsibility coverage. Ethics pupils argue this expert obligation encompasses deciding on insurance kinds and bounds suitable to character exercise dangers, no longer simply sporting minimal required coverage to meet regulatory compliance.

Specialty nursing corporations such as the Emergency Nurses Association, Association of periOperative Registered Nurses, and Oncology Nursing Society put up function statements addressing expert legal responsibility coverage pointers for his or her respective exercise regions. These distinctiveness-unique pointers frequently cope with specific dangers inherent to specific nursing roles, recommending insurance limits and coverage functions aligned with documented declare frequency and severity styles inside every distinctiveness. Reviewing applicable distinctiveness company steerage gives treasured insights for nurses practicing in high-danger regions in which trendy insurance pointers might also additionally show inadequate.

Conclusion

Selecting among claims-made and prevalence-primarily based totally expert legal responsibility coverage calls for cautious evaluation of character profession circumstances, economic considerations, and danger tolerance stages instead of making use of widespread pointers throughout all nursing exercise situations. Claims-made rules provide economic accessibility via decrease preliminary rates and graduated price structures, making expert legal responsibility safety potential for budget-aware nurses inclined to control coverage continuity necessities and eventual tail insurance obligations.

Occurrence-primarily based totally insurance gives simplicity, predictability, and everlasting safety specially treasured for nurses looking forward to professional transitions, distinctiveness changes, or drawing close retirement timelines in which tail insurance charges may in any other case create massive economic burdens. Understanding the essential variations among those insurance structures, spotting ability gaps and vulnerabilities inherent to every type, and matching coverage choice to unique profession tiers and exercise styles allows nurses to steady ultimate expert safety aligned with character desires and circumstances.

Whether deciding on employer-supplied insurance, shopping character rules, or combining each safety layers, knowledgeable decision-making concerning claims-made as opposed to prevalence coverage kinds represents a vital expert duty that safeguards each nursing careers and the economic protection nurses’ paintings at some point of their expert lives to set up and maintain.

FAQs

FAQ 1: Can I switch from a claims-made policy to an occurrence policy without losing coverage?

Yes, however you need to buy tail insurance on your claims-made coverage length to preserve safety for incidents going on for the duration of that timeframe, as switching providers on my own creates everlasting insurance gaps.

FAQ 2: Does agency-supplied malpractice coverage maintain once I depart my activity?

No, agency-supplied claims-made insurance terminates upon employment conclusion, requiring tail insurance buy to preserve safety for incidents going on for the duration of your employment length, even though claims emerge years later.

FAQ 3: Which coverage fees much less over a whole nursing career?

Claims-made rules with tail insurance at retirement usually price 15-25 percentage points much less general than prevalence insurance over 30-yr careers, although common activity adjustments can opposite this gain because of a couple of tail insurance purchases.

FAQ 4: Do I want private legal responsibility coverage if my agency gives insurance?

Many danger control specialists endorse supplemental private insurance due to the fact agency rules might not cowl moonlighting, volunteer work, or claims exceeding coverage limits, and that they terminate while employment ends requiring steeply priced tail insurance.

Read More:

https://nurseseducator.com/didactic-and-dialectic-teaching-rationale-for-team-based-learning/

https://nurseseducator.com/high-fidelity-simulation-use-in-nursing-education/

First NCLEX Exam Center In Pakistan From Lahore (Mall of Lahore) to the Global Nursing

Categories of Journals: W, X, Y and Z Category Journal In Nursing Education

AI in Healthcare Content Creation: A Double-Edged Sword and Scary

Social Links:

https://www.facebook.com/nurseseducator/

https://www.instagram.com/nurseseducator/

https://www.pinterest.com/NursesEducator/

https://www.linkedin.com/company/nurseseducator/

https://www.linkedin.com/in/afzalaldin/

https://www.researchgate.net/profile/Afza-Lal-Din

https://scholar.google.com/citations?hl=en&user=F0XY9vQAAAAJ