Understand what drives Nurse Practitioner Insurance Costs 2027: What Affects Your Premiums? Nurse practitioner coverage fees. Explore the important elements affecting your malpractice charges and a way to get the first-rate insurance for less.

Nurse Practitioner Insurance Costs 2027: What Affects Your Premiums?

Introduction

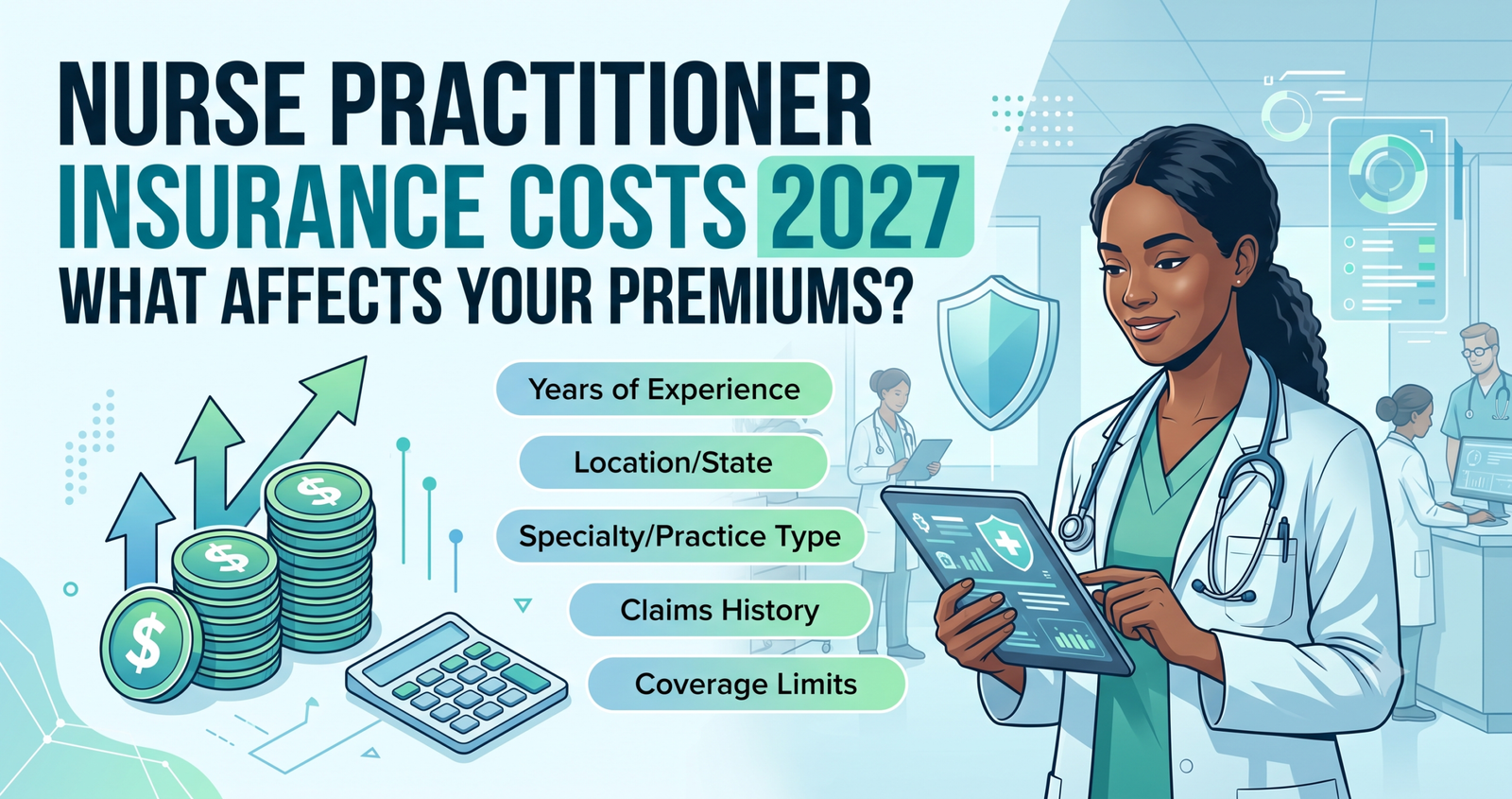

One of the most sensible questions each nurse practitioner asks while shopping expert legal responsibility insurance is likewise one of the maximum nuances: how a lot is that this surely going to feed me? The solution is not often straightforward, due to the fact nurse practitioner coverage fees are not decided with the aid of using an unmarried constant rate. Instead, your top rate displays a complicated calculation constructed on a couple of intersecting variables — your distinctiveness, your location, your claims history, your exercise setting, and numerous different elements that insurers weigh cautiously earlier than quoting you a number.

Understanding precisely what drives the ones calculations places you in a miles more potent role to locate complete insurance on the maximum aggressive feasible price. This manual breaks down each most important top rate thing in clear, actionable element so that you can method the coverage market as a knowledgeable expert.

How Malpractice Insurance Premiums Are Calculated

The Actuarial Foundation of Healthcare Liability Pricing

Insurance businesses do now no longer set charges arbitrarily. Every quote you obtain is grounded in actuarial records — statistical evaluation of ancient claims patterns, common declare severity, litigation frequency with the aid of using distinctiveness and geography, and projected destiny threat throughout populations of comparable practitioners. Insurers examine years of claims records precise to nurse practitioners and use that statistics to assign every applicant a threat profile that immediately determines their top rate.

Understanding this actuarial basis is critical as it shifts the communique from “why is my top rate so high?” to “what precise threat elements in my profile are using this number?” Once you recognize the variables, you benefit from the capacity to actively control a number of them in methods that meaningfully lessen your long-time period coverage fees.

The Role of Coverage Limits in Premium Determination

Before inspecting the practitioner-precise elements that influence your top rate, it is miles critical to recognize how your preferred insurance limits independently affect your fee. The better the in step with-prevalence and combination limits you select, the more the insurer`s ability economic exposure — and consequently the better your top rate.

The enterprise well known for nurse practitioners is $1 million in step with prevalence and $three million in combination. Selecting limits above this threshold, such as $2 million in step with prevalence and $6 million combination, will boom your top rate proportionally. Conversely, a few low-threat exercise environments may also permit decrease limits, although lowering insurance under the usual threshold is normally inadvisable given the unpredictable nature and ability severity of healthcare legal responsibility claims.

Claims-Made vs. Occurrence Policies and Their Premium Implications

The structural form of coverage you pick out has an immediate and considerable effect on your annual top rate, especially within the early years of insurance. Class-made coverage generally begins off evolved with decrease preliminary charges that growth incrementally every 12 months as your insurance matures, finally attaining what insurers name a mature charge after about 5 years.

Incidence coverage contains a better however, constant annual top rate from the outset, reflecting the broader, greater everlasting safety it provides. Over a complete career, the whole fee distinction among those coverage sorts is frequently much less dramatic than the 12 months-one contrast suggests — and the advanced long-time period safety of an incidence coverage regularly justifies the better preliminary funding for maximum nurse practitioners.

How Your Clinical Specialty Drives Insurance Costs

High-Risk Specialties and Their Premium Ranges

Clinical area of expertise is constantly the unmarried maximum influential element in figuring out nurse practitioner malpractice coverage fees. Insurers classify NP specialties via means of their historic claims frequency and common declare severity, and people classifications translate immediately into tiered top rate structures.

Specialties related to the very best malpractice coverage fees for nurse practitioners generally consist of the subsequent exercise regions, indexed with their fashionable annual top rate ranges:

- Psychiatric Mental Health NPs (PMHNPs): $2,500 to $6,000 in step with 12 months, pushed via way of means of excessive charges of affected person self-damage litigation and complicated duty-of-care obligations

- Women`s Health and OB-GYN NPs: $2,000 to $5,500 in step with 12 months, reflecting the excessive declare severity related to obstetric headaches and reproductive fitness decisions

- Acute Care and Emergency NPs: $3,000 to $7,000 in step with 12 months, given the excessive-acuity affected person populace and fast decision-making environment

- Pediatric NPs: $2,000 to $4,500 in step with 12 months, as claims regarding minors regularly appeal to better jury awards

- Family Nurse Practitioners (FNPs): $1,500 to $4,000 in step with 12 months, reflecting the large scope and various affected person populace of number one care exercise

Lower-Risk Specialties and Corresponding Premium Advantages

Not all nurse practitioner specialties bring equal malpractice hazard and decrease-hazard exercise regions advantage from meaningfully decreased top rate fees. NPs practicing in those regions experience a considerable fee gain while buying legal responsibility insurance.

Occupational fitness NPs, aesthetic and beauty NPs, and case control NPs usually constitute the decrease give up of the malpractice top class spectrum, with annual prices often falling in the $800 to $2,000 variety relying on different man or woman factors. The decreased top class displays each the decrease acuity of medical interactions and the traditionally decrease claims frequency in those exercise environments.

Dual Certification and Its Impact on Premium Calculation

Nurse practitioners who keep certifications in a couple of specialties, or who exercise throughout multiple medical areas, face a greater complicated top-class calculation than single-strong point NPs. Insurers normally verify your top class primarily based totally at the highest-chance strong point on your exercise profile in place of averaging throughout your certifications.

An approach that a psychiatric intellectual fitness NP who additionally affords number one care offerings will likely be rated on the better PMHNP top class stage for his or her whole coverage in place of receiving a combined rate. Understanding this calculation is essential while comparing whether dual-strong point exercise is financially based on your typical expert chance profile.

Geographic Location and State-Level Factors

How State Litigation Climate Affects Your Premium

Your country of exercise exerts an effective impact in your malpractice coverage top class that many nurse practitioners substantially underestimate. States fluctuate dramatically in their litigation climate — the frequency with which healthcare vendors are sued, the common length of jury awards and settlements, and the general price of walking prison protection in that jurisdiction.

States traditionally related to better litigation prices and large jury awards — inclusive of New York, California, Florida, Illinois, and Pennsylvania — continuously produce better malpractice charges for nurse practitioners practicing inside them. Conversely, states with tort reform law, harm caps, or decrease litigation frequency normally provide greater favorable top-class environments.

The Impact of State Scope of Practice Laws

The diploma of exercise autonomy granted to nurse practitioners below country regulation additionally impacts top class calculations in approaches that are not constantly straight away intuitive. States that supply NPs complete exercise authority — permitting impartial exercise without doctor collaboration or supervision requirements — can also additionally see barely better charges in a few strong point categories, reflecting the more impartial medical obligation that complete exercise authority entails.

In states with constrained exercise fashions requiring doctor collaboration or supervision, a few insurers view the oversight shape as a partial chance mitigation factor that could modestly affect top class calculations in sure strong point categories. Staying knowledgeable approximately your country`s evolving scope of exercise law is consequently now no longer most effective an expert duty, however a financially applicable one as well.

Multi-State Practice and Telehealth Premium Considerations

The developing occurrence of telehealth exercise and multi-kingdom licensure via the NP Compact creates extra top-class complexity for nurse practitioners who offer care throughout kingdom lines. If you exercise telehealth and serve sufferers in more than one states, your insurer wishes to know — due to the fact your top class and insurance phrases may also want to mirror the litigation weather and regulatory surroundings of each kingdom in that you offer medical services.

Some insurers provide trustworthy multi-kingdom insurance endorsements that expand your coverage throughout all states wherein you preserve licensure. Others require separate regulations or fee extra rates for every extra kingdom of exercise. Confirming this insurance element earlier than signing any coverage is vital for any NP training inside the cutting-edge telehealth surroundings.

Practice Setting and Employment Status

Independent vs. Employed Practice Premium Differences

Your employment and exercise shape is one of the maximum big top-class determinants after strong point and geography. Nurse practitioners in impartial or solo exercise continually pay better malpractice rates than the ones hired inside large healthcare organizations, for numerous interconnected reasons.

Independent NPs deliver the total weight of medical decision-making without institutional hazard control infrastructure, oversight protocols, or shared liability. They also are much more likely to be the named number one defendants in a malpractice declaration in preference to certainly considered one among numerous defendants, which include a bigger institutional employer. Insurers replicate this expanded publicity with inside the top class they assign to independently training nurse practitioners.

High-Volume Practice and Its Relationship to Premium

The quantity of sufferers you notice is every other issue that insurers keep in mind whilst calculating your top class, although it’s influenced is greater variable throughout carriers than strong point or geography. The essential actuarial good judgment is trustworthy: the greater medical encounters you have, the extra the statistical opportunity of a destructive occasion or affected person criticism springing up out of your exercise.

Some insurers ask immediately approximately your annual affected person quantity at some point of the utility method and use statistics to refine your hazard profile. High-quantity number one care NPs or pressing care NPs seeing big numbers of sufferers each day may also come across modestly better rates than their lower-quantity colleagues training with inside the identical strong point and kingdom.

Moonlighting, Volunteer Work, and Secondary Employment

Many nurse practitioners interact in moonlighting, volunteering at network fitness events, imparting locum tenens services, or maintaining secondary employment in medical settings past their number one exercise. Each of those sports represents extra medical publicity that your number one malpractice coverage may also or might not cowl relying on its precise phrases.

Undisclosed secondary medical sports can create risky insurance gaps that most effectively come to be obvious whilst a declaration arises from the one’s sports. Always reveal the total scope of your medical exercise on your insurer and verify explicitly that each place in that you offer affected person care is included below your coverage. Additional medical roles may also modestly boom your top class, however, offers entire safety throughout your complete expert footprint.

Claims History and Experience Level

How Prior Claims Affect Your Insurability and Premium

Your non-public claims records are one of the maximum direct top class influencers to be had to insurers, and its effect may be good-sized and long-lasting. A previous malpractice declared even one which becomes in the end resolved to your favor — alerts increased danger to insurers and normally consequences in better rates, extra underwriting scrutiny, or in a few cases, issue acquiring insurance from sure providers.

The severity and results of previous claims count considerably on this calculation. An unmarried disregarded declaration from early to your profession includes much less long-time period top class effect than a declaration that led to a large agreement or jury award. Insurers additionally don’t forget the character of the declaration whether it meditated a systemic documentation issue, a prescribing blunders pattern, or an remote incident while assessing what it well-known shows approximately your ongoing danger profile.

The Experience Factor: New vs. Seasoned NPs

Newly licensed nurse practitioners and skilled NPs are assessed in another way with the aid of using malpractice insurers, and the connection among enjoyment and top class is greater nuanced than an easy seniority cut price. In the early years of NP exercise, a few insurers view more recent practitioners as better danger because of confined unbiased medical enjoy, at the same time as others see new NPs as decrease danger due to the fact their confined exercise records method no previous claims on report.

As you acquire years of claims-unfastened exercise, maximum insurers praise that tune report with strong or modestly declining rates over the years. Maintaining smooth claims records through rigorous documentation practices, robust affected person communication, and proactive danger control is consequently each a medical and monetary precedence all through your profession.

Strategies to Reduce Your Nurse Practitioner Insurance Costs

Leveraging Professional Association Memberships

One of the maximum trustworthy and continually powerful techniques for decreasing your nurse practitioner malpractice top class is pursuing insurance through your expert nursing association. Organizations along with the American Association of Nurse Practitioners (AANP), the American Nurses Association (ANA), and specialty-particular institutions have negotiated institution prices with main insurers that often supply 10% to 25% top class discounts as compared to character marketplace prices.

Association club additionally presents get entry to danger control training, felony session resources, and persevering with training possibilities that independently lessen your medical legal responsibility exposure — growing a compounding shielding impact that extends properly past the top class cut price alone.

Bundling Coverage and Maintaining Loyalty Discounts

Many malpractice insurers provide multi-coverage reductions for nurse practitioners who package expert legal responsibility insurance with extra merchandise inclusive of popular legal responsibility, cyber legal responsibility, or enterprise owner`s regulations through the equal insurer. If you use an unbiased exercise, requiring a couple of insurance types, bundling through an unmarried provider can generate significant annual savings.

Similarly, keeping long-time relationships with an unmarried insurer and demonstrating a steady claims-unfastened record frequently qualifies you for loyalty pricing and renewal reductions that praise your tune report. Jumping among insurers at each renewal in pursuit of marginally decrease preliminary rates might also additionally fee greater over the years with the aid of forfeiting those amassing loyalty benefits.

Investing in Risk Management Education

Some malpractice insurers provide top rate credit or reductions to nurse practitioners who entirely accepted hazard control persevering with schooling applications. These applications cowl medical documentation pleasant practices, affected person communique strategies, prescribing protection protocols, and different competencies that immediately lessen the probability of a malpractice declare springing up out of your exercise.

Completing hazard control schooling is consequently a twin investment — it makes you a more secure, greater defensible clinician even as concurrently lowering the yearly price of the coverage that protects you. Check together with your insurer at every renewal whether accepted hazard control guides qualify you for a top rate credit score in the imminent coverage year.

Conclusion

Understanding what drives nurse practitioner coverage charges transforms top rate purchasing from a confusing, price-pushed exercising right into a strategic expert decision. Your specialty, location, exercise setting, claims history, insurance structure, and medical quantity all engage to provide your precise top rate — and numerous of these variables are inside your energetic control.

Start by inquiring for comparative costs from as a minimum 3 main NP malpractice insurers, disclosing the overall scope of your exercise actually and completely. Explore affiliation club reductions, verify that each thing of your medical pastime is covered, and make investments with inside the hazard control schooling that makes you each a more secure clinician and a greater appealing coverage hazard. If this manual clarified the top rate elements that rely maximum in your exercise, percentage it with a colleague navigating the equal selections and depart a remark together with your questions. Explore our platform for added sources designed to assist nurse practitioners at each degree of expert exercise.

FAQs

What is the common price of nurse practitioner coverage?

The common annual malpractice coverage price for a nurse practitioner tier from approximately $1,000 to $7,000 in step with year, relying closely on specialty, country of exercise, insurance limits, and exercise setting. Primary care and decrease-hazard specialties fall towards the decrease stop of this range, even as acute care, psychiatric, and obstetric NPs commonly pay charges towards the better stop.

Does my specialty really make that big a difference in my nurse practitioner insurance premium?

Yes, scientific forte is always one of the maximum large top-class determinants for nurse practitioners. High-threat specialties together with psychiatric intellectual fitness, acute care, and women`s fitness bring drastically better charges than decrease-acuity specialties, reflecting the historic frequency and severity of malpractice claims in the ones exercise areas.

Can I decrease my nurse practitioner malpractice coverage expenses without decreasing my insurance?

Absolutely. Joining an expert nursing affiliation for institution fee discounts, retaining a claims-loose exercise history, bundling more than one insurance kind with one insurer, and finishing permitted threat control persevering with training are all validated techniques for decreasing your top class without compromising the intensity of your insurance.

Does working towards more than one state boom my nurse practitioner coverage expenses?

Yes, multi-country exercise — together with telehealth offerings supplied to sufferers in different states — can boom your malpractice top class due to the fact your insurer needs to account for the litigation weather and regulatory surroundings of each country wherein you offer scientific care. Always expose multi-country exercise pastime on your insurer and affirm that your coverage explicitly covers each jurisdiction in that you serve sufferers.

Read More:

https://nurseseducator.com/didactic-and-dialectic-teaching-rationale-for-team-based-learning/

https://nurseseducator.com/high-fidelity-simulation-use-in-nursing-education/

First NCLEX Exam Center In Pakistan From Lahore (Mall of Lahore) to the Global Nursing

Categories of Journals: W, X, Y and Z Category Journal In Nursing Education

AI in Healthcare Content Creation: A Double-Edged Sword and Scary

Social Links:

https://www.facebook.com/nurseseducator/

https://www.instagram.com/nurseseducator/

https://www.pinterest.com/NursesEducator/

https://www.linkedin.com/company/nurseseducator/

https://www.linkedin.com/in/afzalaldin/

https://www.researchgate.net/profile/Afza-Lal-Din

https://scholar.google.com/citations?hl=en&user=F0XY9vQAAAAJ