Discover When to Buy Malpractice Insurance in Your Nursing Career: 5 Critical Career Stages Every Nurse Must Know in 2026. Precisely whilst shopping for malpractice coverage throughout five nursing profession degrees in 2026 — from scholar rotations to superior exercise and beyond.

When to Buy Malpractice Insurance in Your Nursing Career: 5 Critical Career Stages Every Nurse Must Know in 2026

Introduction

Malpractice coverage is one of the maximum consequential — and maximum overlooked — monetary choices in a nursing profession. In 2024, 12,655 registered nurses had been named in malpractice claims, and common indemnity payouts for nurse practitioners reached a record $332,137, in step with the 2024 CNA/NSO Nurse Practitioner Professional Liability Exposure Claim Report. Yet many nurses continue to be underinsured at each degree in their careers, frequently counting on employer-furnished insurance that contains important gaps. Understanding exactly whilst to achieve non-public malpractice coverage — and what type — is now no longer optional. It is a foundational act of expert self-protection.

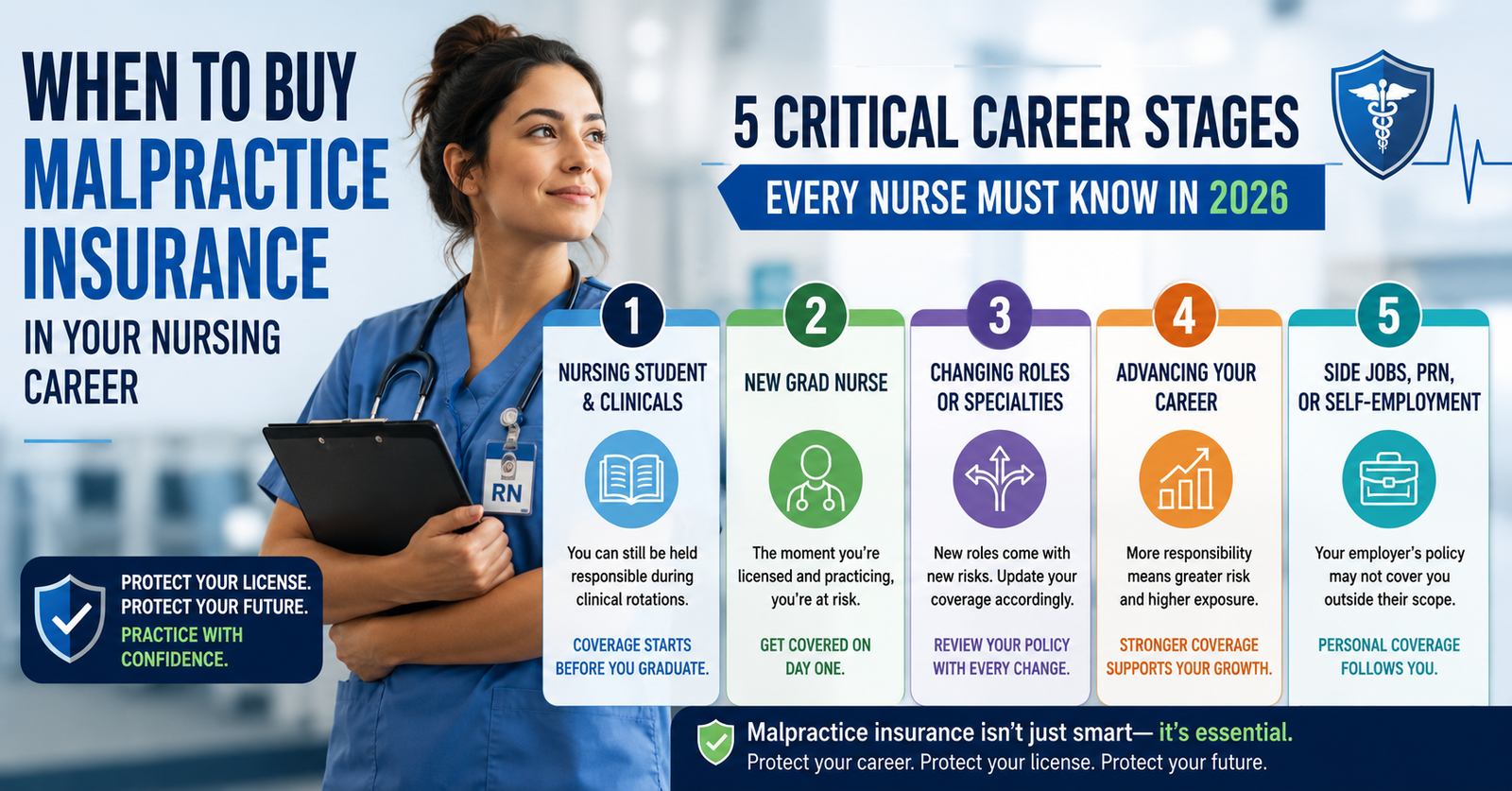

Stage 1: Nursing Students — Before Your First Clinical Day

The query of whilst to buy malpractice coverage has a clear, evidence-primarily based totally solution for nursing college students: earlier than your first actual medical rotation. According to the American Nurses Association (ANA, 2024), all nursing college students must convey character expert legal responsibility insurance — unbiased of any institutional coverage — previous to their first medical day. This advice displays a developing popularity that nursing college students are increasingly assigned to higher acuity affected person care environments in advance of their training, growing actual prison publicity lengthy earlier than graduation.

Many college students incorrectly expect that their nursing school`s institutional insurance or their medical facility’s umbrella coverage absolutely protects them. In maximum cases, those regulations defend the group first — now no longer the character scholar. Fortunately, scholar nurse malpractice coverage is some of the maximum low-priced expert insurance to be had anywhere.

As of 2024, the Nurses Service Organization (NSO), one of the nation’s biggest and maximum authentic nursing legal responsibility providers, gives scholar nurse insurance for as little as $35 in step with 12 months for up to $1 million in step with incidence and $6 million in combination insurance. According to the National Student Nurses’ Association (NSNA) 2024 annual survey, about 68% of nursing college students now convey character expert legal responsibility insurance — a substantial growth in current years, although nonetheless leaving almost 1-0.33 of college students unprotected.

Even with inside the occasion of a frivolous declaration, the price of prison protection on my own may be devastating. The National Practitioner Data Bank reviews that the common price to guard a nursing malpractice declares exceeds $45,000 — no matter outcome. For a scholar whose handiest earnings is a part-time job, that threat is honestly now no longer acceptable.

Stage 2: New Graduate Nurses — the Most Vulnerable Transition Point

The length at once following commencement and earlier than the primary day of employment represents one of the highest-chance home windows in a nursing career. New graduate nurses who’ve simply surpassed the Next Generation NCLEX-RN (NGN) however have now no longer but commenced their first role exist in a criminal grey area — they preserve a license however can also additionally haven’t any enterprise insurance in place. Any medical hobby at some point of this length, together with volunteer care, casual nursing assistance, or network fitness events, is unprotected.

New graduate RNs getting into clinic employment must now no longer count on enterprise insurance is entire or permanent. Employer-furnished malpractice guidelines in without a doubt all healthcare settings are claims made through default. This shape manner that if a declare is filed after a nurse leaves that enterprise — even for an incident that passed off years in advance at some point of that employment — the nurse can be absolutely unprotected except tail insurance is bought separately. Employers are not obligated to offer or fund tail insurance whiles a nurse adjusts jobs.

Additionally, enterprise guidelines nearly universally exclude Board of Nursing proceedings and disciplinary proceedings — the maximum not unusual place criminal danger nurses absolutely face in practice. In 2026, hiring a private license protection lawyer for a Board of Nursing research charges upward of $10,000 out of pocket. Individual expert legal responsibility insurance with license safety provisions converts that doubtlessly career-finishing economic disaster right into a viable process. For new graduate RNs, private malpractice coverage normally charges between $one hundred and $three hundred annually — a modest funding given the size of chance it addresses.

Stage 3: Experienced RNs, Specialty Nurses, and High-Acuity Roles

As nurses improve of their careers and pass into uniqueness roles — together with in depth care, emergency nursing, exertions and delivery, pediatrics, oncology, and perioperative care — their criminal chance profile will increase substantially. High-acuity medical environments contain complicated decision-making, speedy deteriorating affected person conditions, and high-stakes interventions wherein mistakes will have intense consequences. These specialties bring statistically better malpractice declare rates, and nurses working towards them advantage maximum from occurrence-primarily based totally coverage guidelines.

The difference among claims-made and occurrence-primarily based very insurance turns into severely essential for skilled nurses who alternate employers, tackle in step with Diem shifts, or paintings throughout more than one center. An occurrence-primarily based totally coverage covers any incident that happened at some stage in the coverage period, irrespective of while a declaration is officially filed — even years or many years later.

Claims-made coverage, via way of means of contrast, covers best claims filed at the same time, as the coverage is lively. If a nurse with a claim-made coverage modifications jobs or retirees, any declaration filed in a while is unprotected until tail insurance is purchased. According to a 2026 evaluate via way of means of MEDPLI, tail insurance normally fees two hundred to 250 percent of the expiring annual premium — paid as a lump sum — and isn’t always a duty any organization is needed to fulfill.

Travel nurses face the maximum acute model of this challenge. As unbiased contractors working throughout more than one center and jurisdictions, tour nurses often have constrained or time-constrained business enterprise insurance, that applies best at the same time as beneath lively contract. According to Insureon, organization regulations do now no longer cowl nurses operating as unbiased contractors at all, making private malpractice coverage now no longer simply beneficial however professionally vital for all and sundry operating with inside the tour or in step with diem nursing sector.

Stage 4: Advanced Practice Registered Nurses (APRNs) Highest Risk, Highest Stakes

No organization of nursing specialists faces extra felony publicity than Advanced Practice Registered Nurses (APRNs) — along with Nurse Practitioners (NPs), Certified Registered Nurse Anesthetists (CRNAs), Clinical Nurse Specialists (CNSs), and Certified Nurse-Midwives (CNMs). As APRNs tackle improved diagnostic and prescriptive authority, their scope of exercise more overlaps with that of physicians — and their publicity to malpractice claims grows proportionally.

The 2024 CNA/NSO Nurse Practitioner Professional Liability Exposure Claim Report documented that the common NP malpractice indemnity fee reached a record $332,137 — the best discerns ever recorded. Meanwhile, almost 1/2 of all malpractice charges rose among 2023 and 2024 in keeping with American Medical Association data. NPs getting into their first role upon certification ought to steady person malpractice insurance earlier than seeing their first patient — now no longer after. Every APRN organization-furnished cover ought to be scrutinized: does it observe the nurse or the organization? Does it cowl Board of Nursing proceedings? Does it offer the nurse with unbiased felony illustration if the institution`s hobbies struggle with theirs?

APRNs in states with complete exercise authority that open unbiased or collaborative practices bring a particularly crucial want for robust, occurrence-primarily based very private malpractice coverage. The institutional protection internet of medical institution organization insurance disappears completely in personal exercise settings, and the APRN on my own bears complete legal responsibility for each medical selection made. NSO, Proliability (the different AANP-advocated provider), and CM&F Group are a few of the maximum mounted companies of APRN-precise malpractice insurance and need to be evaluated via way of means of each APRN earlier than, no longer after, getting into exercise.

Stage 5: Nurse Educators, Researchers, and Retiring Nurses — Coverage at the End

Malpractice danger does now no longer retire whilst a nurse step lower back from bedside care. Nurse educators who supervise scientific college students in exercise settings bring legal responsibility for the scientific steerage they provide — and maximum educational organization guidelines do now no longer increase good enough person safety to scientific school in all situations. Nursing researchers undertaking research concerning human subjects, or nurses supplying telehealth, consulting, or advisory offerings outdoor of a number one organization relationship, all bring legal responsibility exposures that non-public malpractice coverage should address.

Retiring nurses constitute an often not noted danger group. A nurse who retires from scientific exercise in 2026 can also additionally nonetheless face a malpractice declaration filed years later for an incident that happened during their very last years of employment. If that nurse held claims-made coverage through their organization, and no tail insurance turned into secured at retirement, they face that declaration without coverage whatsoever.

Occurrence-primarily based very non-public guidelines put off this danger entirely — they hold to cowl incidents from the coverage length indefinitely, irrespective of whilst the declaration is filed. Nurses making retirement plans need to evaluate the sort of insurance their organization has supplied and make the right choice approximately buying tail insurance or transitioning to non-public prevalence coverage earlier than their very last day of exercise.

Types of Malpractice Insurance: Choosing the Right Policy at Every Stage

Understanding the two number one coverage systems is important for making a knowledgeable choice at any profession stage. Occurrence-primarily based totally guidelines cowl any incident that takes place during the coverage length, irrespective of whilst a declaration is filed — providing permanent, unconditional safety for the occasions of that length.

Claims-made guidelines are decrease in in advance fee however require non-stop energetic insurance, and upon coverage cancellation or task extrade, disclose the nurse to exposed claims except tail insurance is bought at full-size fee. Occurrence-primarily based totally guidelines are broadly advocated through nursing expert businesses and legal responsibility specialists because the desired shape for long-time period profession safety — mainly for nurses who extrade employers, travel, paintings in line with diem, or are drawing close retirement.

Standard person RN insurance from legit providers, which include NSO, CM&F Group, and Proliability — normally tiers from $85 to $one hundred sixty-five in line with yr for $1 million in line with prevalence and $6 million in mixture insurance limits. This fee is discreet relative to the economic and expert danger it protects against, and it consists of the vital advantage of unbiased criminal representation — safety organization guidelines are structurally not able to guarantee.

Conclusion

The selection of while to shop for malpractice coverage in a nursing profession has one constant solution throughout each stage: in advance, than you observed you want it. From the primary scientific rotation as a nursing pupil — at as little as $35 in keeping with yr — to the accelerated authority of an APRN in impartial practice, to the very last day of a retiring bedside nurse`s profession, character expert legal responsibility insurance is a profession-lengthy funding in expert survival.

Employer insurance is not often sufficient, Board of Nursing complaints are by no means included, and the economic outcomes of unprotected claims may be catastrophic and everlasting. Every nurse — pupil, new graduate, specialist, superior practitioner, educator, or retiree — merits the entire safety that informed, personally bought malpractice coverage affords.

FAQs

Does my organization’s malpractice coverage absolutely defend me as a nurse?

No. Employer-supplied guidelines in the main defend the institution, now no longer the character nurse. They are nearly constantly claims-made guidelines that quit while employment ends, and that they almost universally exclude Board of Nursing disciplinary complaints — which require separate, impartial criminal illustration that most effective non-public malpractice insurance affords.

What is the distinction among occurrence-primarily based totally and claims-made malpractice coverage for nurses?

An occurrence-primarily based totally cover covers any incident that occurred at some stage in the coverage period — even though the declaration is filed years later — imparting everlasting safety without the want for tail insurance. A claims-made coverage most effective covers claims filed at the same time as the coverage stays active; nurses who alternate jobs or retire below claims-made insurance need to buy tail insurance, which normally fees 200–250% of the yearly top class as a lump sum.

When ought to a nursing pupil buy malpractice coverage?

The American Nurses Association recommends that each one nursing college students acquire character expert legal responsibility insurance earlier than their first scientific day. Student nurse guidelines from companies like NSO value as little as $35 in keeping with yr for up to $1 million in keeping with occurrence — making it one of the maximum lower priced protections in any career relative to the danger it covers.

Do Nurse Practitioners want their personal malpractice coverage even though their organization affords insurance?

Yes. NPs face the best malpractice danger of any nursing role, with common indemnity bills accomplishing a record $332,137 in 2024. Employer guidelines regularly exclude Board of Nursing complaints, might not observe the NP in the event that they alternate positions, and location institutional pursuits above the ones of the character practitioner. Every NP ought to bring character occurrence-primarily based totally insurance from a good issuer that includes NSO, Proliability, or CM&F Group — impartial of any organization coverage.

Read More:

https://nurseseducator.com/didactic-and-dialectic-teaching-rationale-for-team-based-learning/

https://nurseseducator.com/high-fidelity-simulation-use-in-nursing-education/

First NCLEX Exam Center In Pakistan From Lahore (Mall of Lahore) to the Global Nursing

Categories of Journals: W, X, Y and Z Category Journal In Nursing Education

AI in Healthcare Content Creation: A Double-Edged Sword and Scary

Social Links:

https://www.facebook.com/nurseseducator/

https://www.instagram.com/nurseseducator/

https://www.pinterest.com/NursesEducator/

https://www.linkedin.com/company/nurseseducator/

https://www.linkedin.com/in/afzalaldin/

https://www.researchgate.net/profile/Afza-Lal-Din

https://scholar.google.com/citations?hl=en&user=F0XY9vQAAAAJ