Discover 9 Dangerous Myths About Nursing Malpractice Insurance Every Nurse Must Stop Believing in 2026. The nine maximum risky myths approximately nursing malpractice coverage in 2026 — and the records that shield each nurse`s license, career, and monetary future.

In 2026 9 Dangerous Myths About Nursing Malpractice Insurance Every Nurse Must Stop Believing

Introduction

Nursing malpractice coverage is one of the maximum misunderstood subjects in expert nursing exercise — and people misunderstandings deliver actual consequences. According to a 2024 evaluation referred to through Nurse.org, 12,655 registered nurses had been named in malpractice claims in 2024 alone, outpacing physicians for the primary time in recorded history.

The National Practitioner Data Bank (NPDB) similarly confirms that over 10,000 destructive moves are taken towards nurses annually, with about 1 in 10 nurses dealing with research for a capacity violation of the Nursing Practice Act throughout their careers. Despite those realities, myths hold to power risky decisions. For nursing students, practicing RNs, superior exercise nurses, and educators alike, setting apart reality from fiction has by no means been greater urgent.

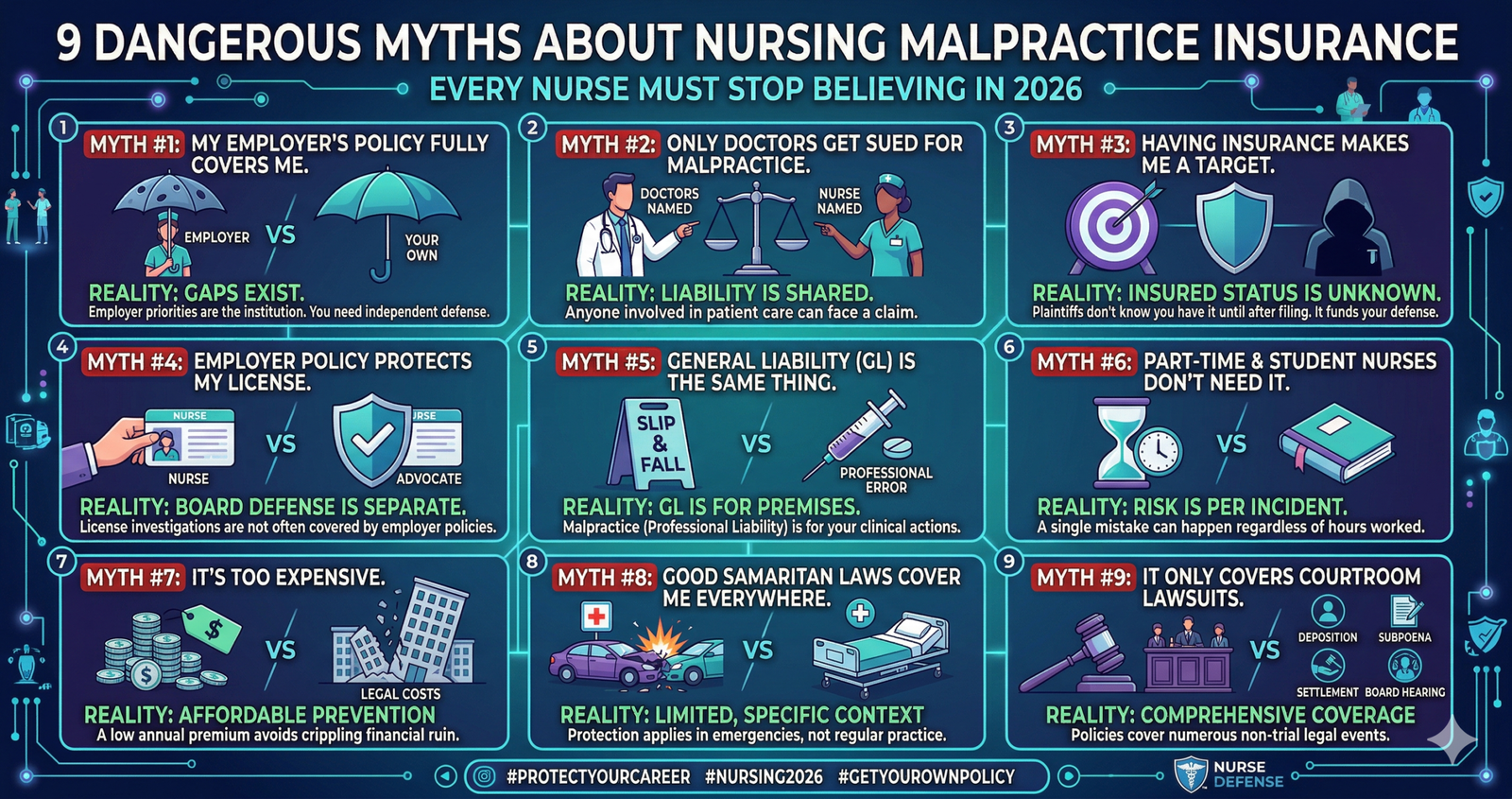

Myth 1: “My Employer’s Insurance Fully Covers Me”

This is the unmarried maximum good sized and professionally risky delusion in nursing today. Most nurses who depend completely on agency insurance have by no means study the coverage, reviewed its exclusions, or requested vital questions on the scope of its protection. According to the American Nurse Journal — the authentic scientific magazine of the American Nurses Association (ANA) — agency coverage continuously has gaps that depart person nurses uncovered in vital situations. If an incident falls out of doors your activity description, happens once you renounce or are terminated, or falls inside coverage exclusion, your agency may also decline to guard you entirely.

More critically, the agency’s coverage corporation represents the institution — now no longer the person nurse. When each clinic and a nurse are named with inside the equal lawsuit, the institutional insurer may also pursue a felony method that shifts legal responsibility towards the person nurse to shield the facility’s monetary interests.

This warfare of hobby is not hypothetical; it is far from a documented sample in nursing legal responsibility litigation. The New York State Nurses Association explicitly warns that agency malpractice coverage “acts with inside the hobby of the agency first,” and that nurses with their very own personal insurance revel in to a drastically more degree of protection.

Myth 2: “Having Malpractice Insurance Makes You a Target for Lawsuits”

This fable is not simplest false — its miles dangerously misleading. The fact is that a nurse`s coverage fame isn’t public information. Whether a defendant holds non-public insurance can simplest are observed after a lawsuit is officially filed, which means no plaintiff’s lawyer can pick out goals primarily based totally on who contains coverage.

Legal specialists and researchers always agree that malpractice coverage does now no longer makes nurses much more likely to be sued. Most complaints stem from perceived negligence, bad affected person results, or verbal exchange failures — now no longer from the presence or absence of coverage. Nurses who are uninsured truly face equal dangers with non-monetary or criminal safety in place.

Myth three: “Nursing Malpractice Insurance Is Too Expensive”

This false impression prevents many nurses from securing safety that is, in fact, remarkably affordable. According to Nurse.org, the common fee of person nursing malpractice coverage is approximately $a hundred in keeping with yr for RNs — roughly $eight in keeping with month. Providers consisting of Nurses Service Organization (NSO), Proliability (previously Marsh), and CNA Healthcare provide incidence-primarily based totally rules for RNs carrying $1 million in keeping with incidence and $6 million mixture limits with inside the variety of $85 to $605 yearly.

APRNs with prescriptive authority face better premiums — generally between $three hundred and $1, two hundred yearly relying on strong points and states however even the ones figures are modest in comparison to the monetary publicity they cover. With the common clinical malpractice declaration paying out over $two hundred, 000, the once-a-year top rate represents extraordinary cost for professional safety.

Myth 4: “Employer Coverage Protects Me During Board of Nursing Investigations”

This is one of the maximum vital gaps nurses fail to recognize. Employer-provided malpractice coverage nearly universally excludes Board of Nursing lawsuits and disciplinary court cases — exactly the maximum not unusual place criminal risk nurses certainly face in daily practice. According to the Nurses Service Organization’s 2023 nurse legal responsibility profile report, license safety movements are an increasing number of being pursued one at a time from civil malpractice claims, which means a nurse can concurrently face board court cases and civil litigation for the equal incident, with every requiring unbiased criminal representation.

In 2025, the common license protection fee rose 18%, from $5,330 in 2020 to $6,304 — charges that organization rules will no longer cover. Only person expert legal responsibility coverage always consists of license safety and Board of Nursing representation.

Myth 5: “I’m a Good Nurse — I’ll Never Be Sued”

Clinical excellence isn`t a crook shield. According to the latest records from Nurse.org’s 2024 malpractice evaluation, registered nurses now face a hazard diploma 2.3 times higher than the countrywide not unusual place due to immoderate affected man or woman volumes and overwhelming workloads. Nurses can be named in lawsuits even though every protocol is found perfectly.

Lawsuits are frequently triggered thru affected man or woman or personal family dissatisfaction, conversation breakdowns, or adverse consequences that are not related to negligence. Patricia Benner’s landmark nursing framework, From Novice to Expert (1984), reminds us that scientific competence should be continuously documented and demonstrated — but documentation on my own cannot prevent a lawsuit from being filed. What it may do is beautify the safety while one occurs.

Myth 6: “Claims-Made Coverage through My Employer Is the Same as Occurrence Coverage”

The distinction among those coverage kinds is one of the maximum consequential — and least understood — differences in nursing coverage. An occurrence-primarily based totally coverage covers any incident that passed off for the duration of the insurance period, no matter while the declare is officially filed — even years or many years later. Class-made coverage, with the aid of using contrast, covers a declaration most effectively while each incident and the formal submitting of the criticism arise even as the coverage is lively with the equal insurer.

Employer-supplied insurance is nearly constantly claims-made. When a nurse adjustments jobs, retires, or is terminated, that insurance ends immediately. Any declare filed afterward — even for an incident that came about years earlier — can be completely unprotected without separate tail insurance. According to a 2025 coverage evaluation with the aid of using MEDPLI, tail insurance commonly expenses two hundred to 250 percentage of the expiring claims-made annual premium, paid as a lump sum — a price employer isn’t obligated to provide.

Myth 7: “Malpractice Insurance Only Matters for Nurses in High-Risk Specialties”

While nurses in exertions and delivery, the emergency department, extensive care, and oncology do convey statistically better malpractice publicity, no nursing function is immune from criminal risk. According to NSO’s 2023 report, almost 1/2 of all malpractice claims contain nurses running in long-time period care (LTC) and domestic fitness settings — environments that many nurses traditionally taken into consideration decrease risk.

Treatment and care-associated claims accounted for 56% of all allegations in nursing domestic settings, with damaging occasions, which include falls, infections, and medicine mistakes regularly ensuing in deadly accidents or intense complications. Nurses who paint in network fitness, ambulatory care, telehealth, or as impartial responsibility nurses additionally face disproportionate publicity because of decreased supervisory infrastructure and documentation challenges.

Myth 8: “Malpractice Insurance Covers Everything — Including Intentional Acts”

All nursing malpractice coverage rules bring exclusions that nurses should recognize earlier than assuming complete insurance. According to Nurse.org, fashionable exclusions consist of cheating or crook acts, sexual misconduct, sexual harassment claims filed with the aid of using patients, and conditions concerning reckless push aside at a part of the nurse.

Intentional torts — along with battery, intentional infliction of emotional distress, or falsification of scientific records — also are excluded from insurance. These aren’t minor part cases; the New York State Nurses Association notes that after a nurse has been observed responsible of an intentional tort, coverage will now no longer cowl the declare irrespective of the coverage type. Understanding what your coverage does now no longer cowl is as crucial as understanding what it does.

Myth 9: “Student Nurses and New Graduates Don`t Need Personal Coverage”

Many nursing college students and newly certified nurse’s expect they may be routinely included with the aid of using their school’s or organization’s umbrella coverage and consequently haven’t any private legal responsibility exposure. This assumption is incomplete and probably dangerous. Student nurses might also additionally face private legal responsibility at some stage in medical rotations in conditions that fall out of doors their academic institution’s insurance boundaries.

New graduates transitioning from their first activity face an insurance hole the instant their claims-made organization coverage terminates. Proliability, NSO, and HPSO all provide less expensive scholar and new graduate rules — a few beginning as low as $35 in step with 12 months — designed to bridge precisely those gaps. Beginning a nursing profession with private malpractice insurance in region from day one is a foundational act of expert responsibility.

Conclusion

Nursing malpractice coverage myths are not innocent misunderstandings — they may be expert liabilities of their personal right. From the fake consolation of depending totally on organization insurance to the harmful perception that exact medical exercise gets rid of criminal risk, every fantasy tested right here represents an actual and documented hole in lots of nurses’ profession safety strategy. The facts are clear: malpractice claims towards nurses are rising, Board of Nursing investigations are increasing, and jury awards are developing in severity.

Yet private expert legal responsibility coverage stays one of the maximum less expensive and highest-cost protections to be had in any profession, averaging just $a hundred in step with 12 months for RNs. For nursing college students getting ready to go into exercise, bedside nurses navigating complicated medical environments, superior exercise nurses handling unbiased caseloads, and nurse educators shaping the following technology of clinicians, wearing man or woman malpractice coverage isn’t always a luxury — it’s miles a non-negotiable pillar of sustainable, legally literate nursing exercise in 2026.

FAQs

Does nursing malpractice insurance cover me when I volunteer outside of my regular job?

Employer-furnished regulations generally exclude expert sports done outdoor your number one employment setting, such as volunteer nursing work, facet employment, and telehealth consultations. Individual non-public legal responsibility coverage regulations normally offer broader insurance that follows you throughout settings, however confirming insurance scope together with your precise issuer earlier than volunteering is essential.

What is the distinction between incidence and claims-made nursing malpractice coverage?

Occurrence regulations cowl any incident that befell at some point of the insurance period, no matter whilst the declare is filed — even years later. Claims-made regulations best cowl claims filed whilst the coverage remains active. If you go away from employment beneath claims-made coverage without shopping tail insurance, incidents out of your earlier employment can be much unprotected.

Will my nursing malpractice coverage shield me if the State Board of Nursing documents a grievance towards me?

Employer-provided coverage nearly by no means covers Board of Nursing investigations or disciplinary proceedings. Individual non-public malpractice coverage regulations from vendors like NSO, Proliability, and HPSO generally consist of license protection insurance — one of the maximum crucial motive’s nurses are cautioned to hold their very own coverage independently of organization insurance.

How do I recognize if my organization`s malpractice coverage is adequate?

Request a replica of your organization’s coverage and evaluation it for exclusions, insurance limits, coverage type (incidence vs. claims-made), and whether or not it explicitly covers Board of Nursing proceedings. Legal specialists from the American Nurse Journal advocate now no longer counting on verbal assurances — the high-quality print of the real coverage report is the best dependable manual to information the authentic scope of your insurance.

Read More:

https://nurseseducator.com/didactic-and-dialectic-teaching-rationale-for-team-based-learning/

https://nurseseducator.com/high-fidelity-simulation-use-in-nursing-education/

First NCLEX Exam Center In Pakistan From Lahore (Mall of Lahore) to the Global Nursing

Categories of Journals: W, X, Y and Z Category Journal In Nursing Education

AI in Healthcare Content Creation: A Double-Edged Sword and Scary

Social Links:

https://www.facebook.com/nurseseducator/

https://www.instagram.com/nurseseducator/

https://www.pinterest.com/NursesEducator/

https://www.linkedin.com/company/nurseseducator/

https://www.linkedin.com/in/afzalaldin/

https://www.researchgate.net/profile/Afza-Lal-Din

https://scholar.google.com/citations?hl=en&user=F0XY9vQAAAAJ